- France’s bonds have been underperforming peers on budget risks

- Investors await S&P credit rating update due on Friday

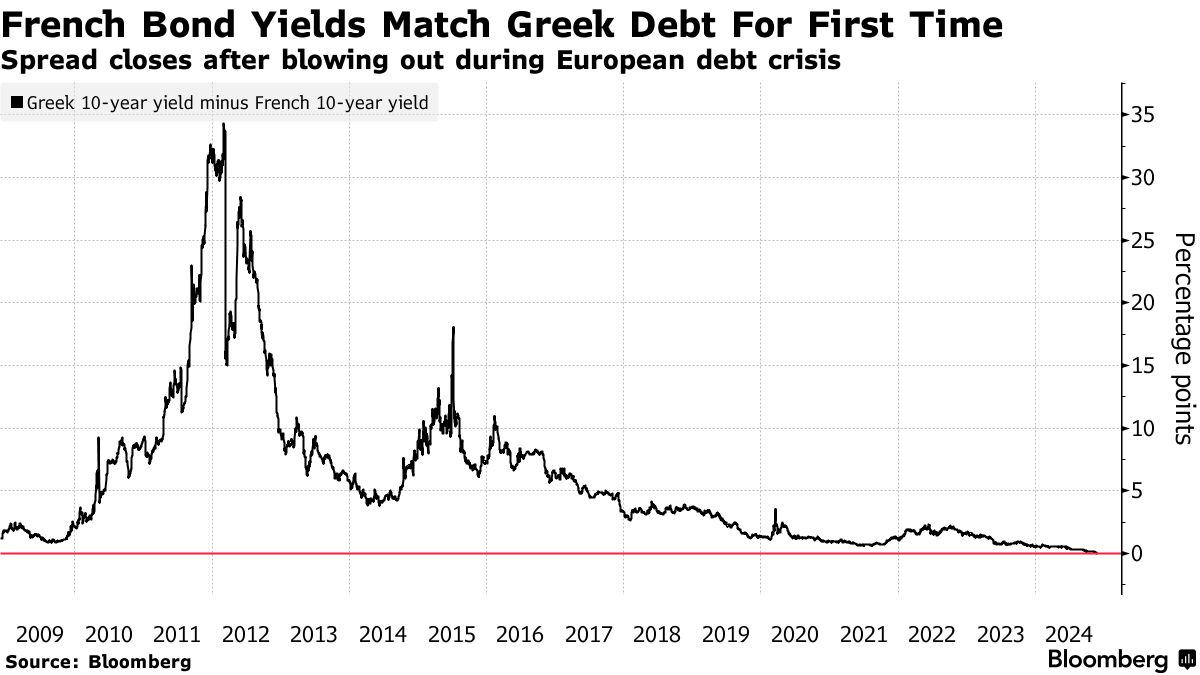

France’s benchmark bond yield matched Greece’s for the first time on record, the latest milestone in a week marked by mounting anxiety over the fate of Prime Minister Michel Barnier’s government.

The rate on 10-year French notes, traditionally considered among the safest in the euro area, briefly rose to 3.03% before paring the move. That was the same as comparable Greek bonds, a country once at the heart of the European sovereign debt crisis.

Investors are concerned that France may struggle to pass a budget for next year, with the far-right National Rally party threatening a no-confidence vote to bring the government down if its demands aren’t met. While French bonds rallied after Finance Minister Antoine Armand said he is prepared to make concessions on the 2025 budget, that did little to dent months of underperformance.

“We are not collapsing, but we risk coming down like a plane at altitude,” Armand said in an interview on RMC radio. “There is a path and it’s this budget.”

Armand didn’t specify the degree of changes the government is willing to make, but he confirmed that Barnier is ready to tweak plans to raise taxes on electricity that Marine Le Pen’s party has slammed. She has also demanded a modification of measures to curb pensions expenditure and reduce state reimbursement of medicines.

The finance minister’s remarks drove French 10-year yields down by as much as six basis points to 2.97% on Thursday and tightened the gap over safer German notes — a key market gauge of risk — to 84 basis points. That’s still 40 basis points above the level seen before President Emmanuel Macron called a snap vote in June, and is near the highest since the euro-area sovereign debt crisis.

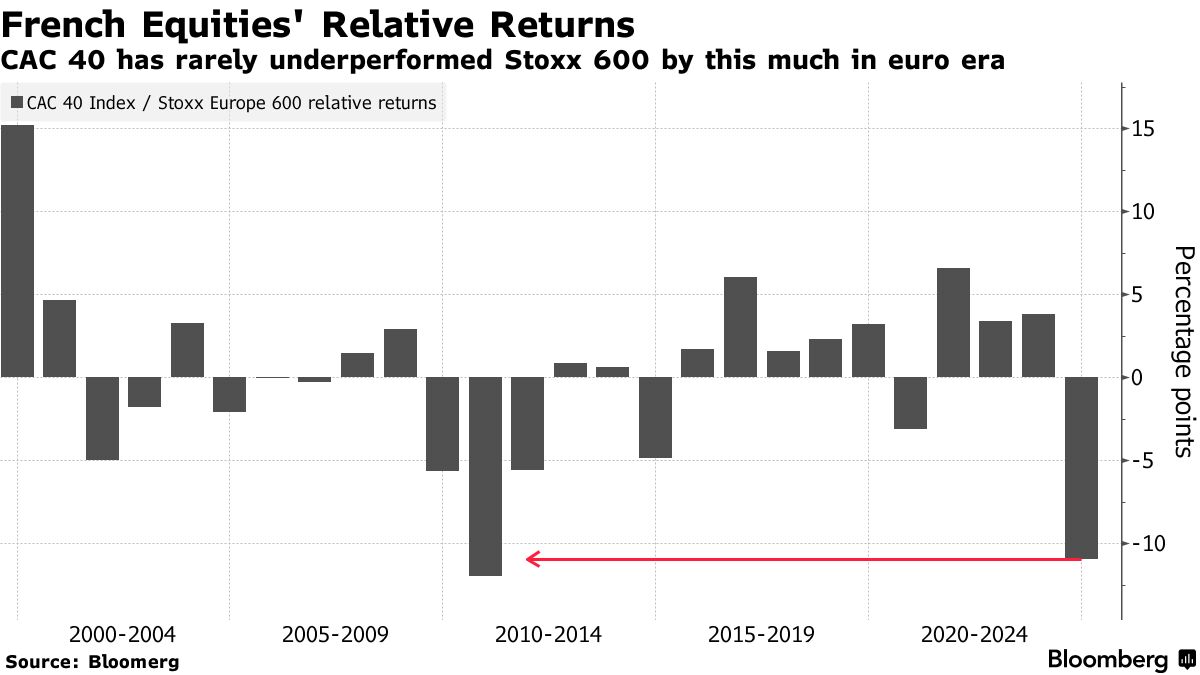

French bonds suffered their worst weekly outflow in more than two years in the five days through Tuesday, according to data compiled by BNY, the world’s largest custodian. The investor exodus has also sent stocks plunging, with the benchmark equity index on track for its worst year relative to European shares since 2010.

Further moves will depend on how the National Rally responds to government proposals for the budget in the coming days and weeks. Barnier’s plan included €60 billion ($63 billion) of spending cuts and tax hikes in an effort to bring the country’s deficit to about 5% of GDP next year, compared with 6.1% expected in 2024.

While the National Rally is not part of the administration, which is mainly made up of Macron’s centrists and Barnier’s conservative Republicans, the party matters because it has enough lawmakers to topple it by supporting a no-confidence vote in parliament alongside the leftist New Popular Front alliance.

Rating Risk

On top of that, S&P Global Ratings is scheduled to update its assessment of France on Friday. Both Fitch Ratings and Moody’s Ratings gave France a negative outlook last month, citing the deterioration of public finances and the political challenges in containing swollen budget deficits.

“The economic outlook for France in the longer term is bleak,” said Michiel Tukker, a senior rates strategist at ING Groep NV. “A weakening French economy will make the already seemingly impossible task of fiscal consolidation even more challenging.”

Investors were already souring on Europe due to the twin threats of US trade tariffs and escalating Russia tensions. Now France is looking like the worst of a bad bunch, meaning that any money that is allocated to Europe will likely go elsewhere.

International investors hold more than half of France’s government debt, according to Banque de France data, and there are already signs that Japanese investors are selling and switching into other European bond markets.

Symbolic Warning

By comparison, Greek assets have been on an upward trajectory as the nation recovers from the euro-area debt crisis, having regained investment-grade status last year. At the peak of Greece’s woes in 2012, its 10-year bonds yielded over 30 percentage points more than French debt.

To be sure, the small size of the Greek bond market makes meaningful comparisons difficult. Greek government debt eligible to a key index amounts to a little over €80 billion, compared to over €1.8 trillion for France.

While France’s Finance Minister Armand downplayed the comparison to Greece, saying his nation’s economy is “far superior,” he acknowledged the need for fiscal restraint.

“We will go through difficult times,” he said. “Other countries — Greece, Italy, Spain — have been through that.”

Yet the fact French yields matched or exceeded three of the four so-called PIGS — the moniker used to describe the region’s crisis-struck economies of Portugal, Italy, Greece and Spain — is a symbolic warning. Some in the market, such as Allianz Global Investors, see a risk French bonds could soon even yield the same as Italy, where 10-year debt now carries just a 40 basis point premium over its neighbor.

“The so-called ‘PIGS’ countries were forced to reform structurally after the European crisis which in the end paid out,” said Sonia Renoult, a senior rates strategist at ABN Amro Bank NV in Amsterdam. “France never undertook such reforms and today they have to pay the bill for it.”

Written by: Greg Ritchie, Julien Ponthus, and William Horobin — With assistance from Michael Msika, Alice Gledhill, and James Hirai @Bloomberg

The post “French 10-Year Borrowing Costs Match Greece’s for First Time” first appeared on Bloomberg