America’s biggest oil companies are warning that global crude markets may be nearing an inflection point of higher prices the longer the Strait of Hormuz stays closed.

Every day the waterway remains shut, the world is using up commercial stockpiles, strategic reserves and crude that was stored in vessels before the US and Israel launched the Iran war, Exxon Mobil Corp., Chevron Corp. and ConocoPhillips said this week.

These supplies have helped mitigate prices over the past two months but are now running short, Chevron Chief Financial Officer Eimear Bonner said in an interview with Bloomberg TV on Friday.

“A lot of the inventory and spare capacity has been depleted already,” she said. “There’s very little of the buffer left.”

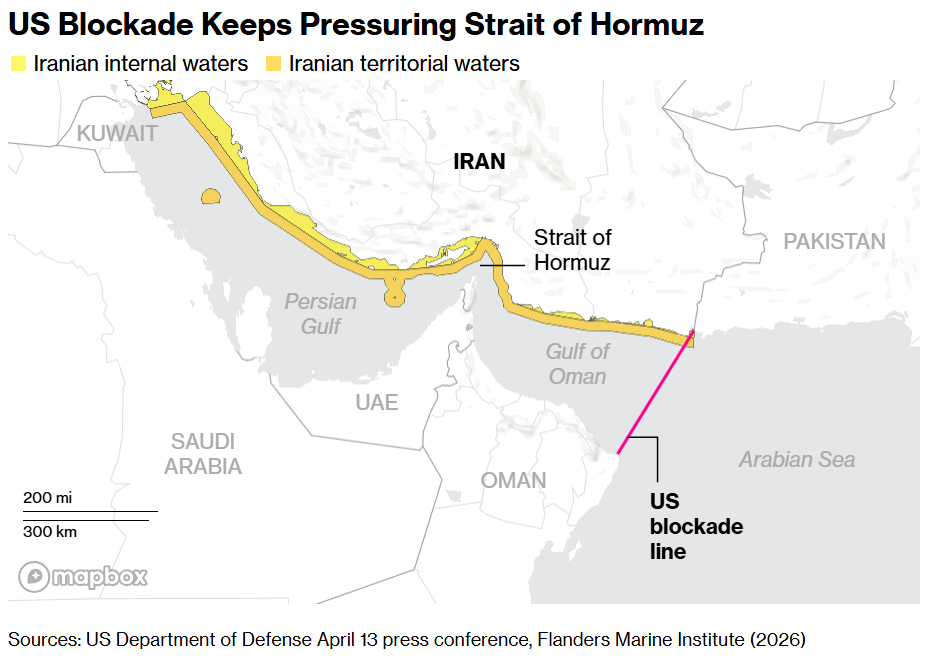

Iran closing the Strait of Hormuz has long been considered a nightmare scenario in energy markets because a fifth of the world’s oil and liquefied natural gas normally passes daily through the chokepoint, which separates the Persian Gulf from open ocean. While prices have climbed more than 50% since Iran effectively closed the waterway two months ago, at just over $100 a barrel, they’re far from record levels.

This could soon change as storage runs out, Exxon CEO Darren Woods said on a call with analysts Friday.

“It’s obvious to most that if you look at the unprecedented disruption and the world’s supply of oil and natural gas, the market hasn’t seen the full impact of that yet,” he said. “There’s more to come if the strait remains closed.”

West Texas Intermediate dropped about 4% to settle around $102 a barrel Friday as Iran signaled readiness to continue diplomatic efforts with the US over the nine-week conflict. Uncertainty over future supplies and messaging from the Trump administration that the Strait will reopen soon have contributed to volatile trading. WTI has jumped more than 50% since the war began.

Crude markets have been in a “grace period” since late February until now because ships loaded before the war take weeks to complete their journeys and so have still been delivering cargoes, ConocoPhillips Chief Financial Officer Andy O’Brien said on call with analysts Thursday.

“Now, all of those have reached their destination,” he said. “The impacts of the lost supply is going to start to become more apparent.”

So far the impact has hit hardest in Asia, where refineries are cutting runs and countries are advising people to drive less and work from home.

“We are going to start to see some import-dependent countries potentially start to face critical shortages as we get into the June-July timeframe,” O’Brien said.

Developed countries’ commercial inventories are on track to reach operational stress levels by early June and hit minimums by September if the strait remains closed, JPMorgan Chase & Co. analysts led by Natasha Kaneva wrote in a note this week. At this point, demand will have to drop further to balance the system, she wrote.

“As you get to the kind of the minimum working levels of inventory on the commercial side, you’re going to lose one of these sources of supply,” Exxon’s Woods said. “We anticipate as that happens in the strait remains closed, that we will continue to see increased prices in the marketplace.”

Written by: Kevin Crowley, David Wethe, and Annmarie Hordern @Bloomberg

The post “Big Oil Bosses Warn Energy Is Moving Closer to Cliff’s Edge” first appeared on Bloomberg

{kind=link}