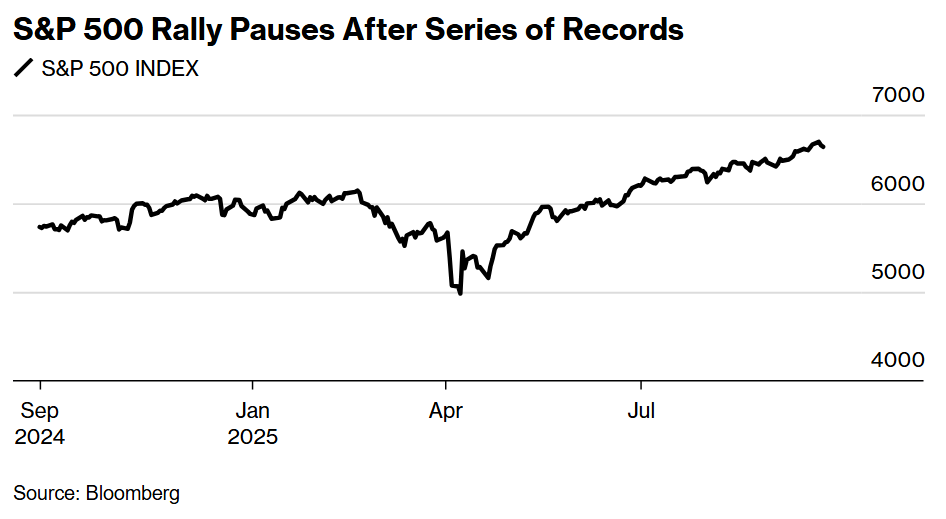

Wall Street’s torrid surge from April’s meltdown is showing signs of exhaustion as stock traders await fresh catalysts amid risks stemming from a labor-market slowdown to sticky inflation.

While the S&P 500 has defied September’s gloomy reputation as the worst month for equity returns, the gauge failed to gain traction on Wednesday. The market ebullience saw the index notching almost 30 records in 2025, eclipsing the average year-end analyst forecast and spurring calls for consolidation.

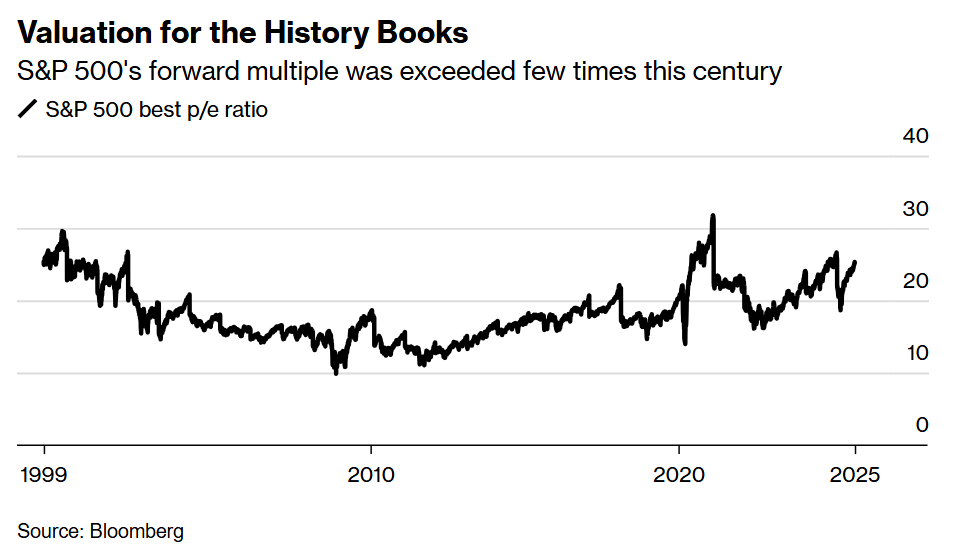

At Bank of America Corp., Savita Subramanian noted that on 19 of 20 metrics, the US equity benchmark is trading at statistically expensive levels.

Bullish investors should keep hedging their portfolios as more and more people chase this year’s stock-market rally, according to Nomura Securities International Inc.’s Charlie McElligott.

Euphoria over AI has turned skeptics into equity buyers at higher levels. This behavior alongside many players at or near maximum exposure has built up downside risk in stocks, he noted.

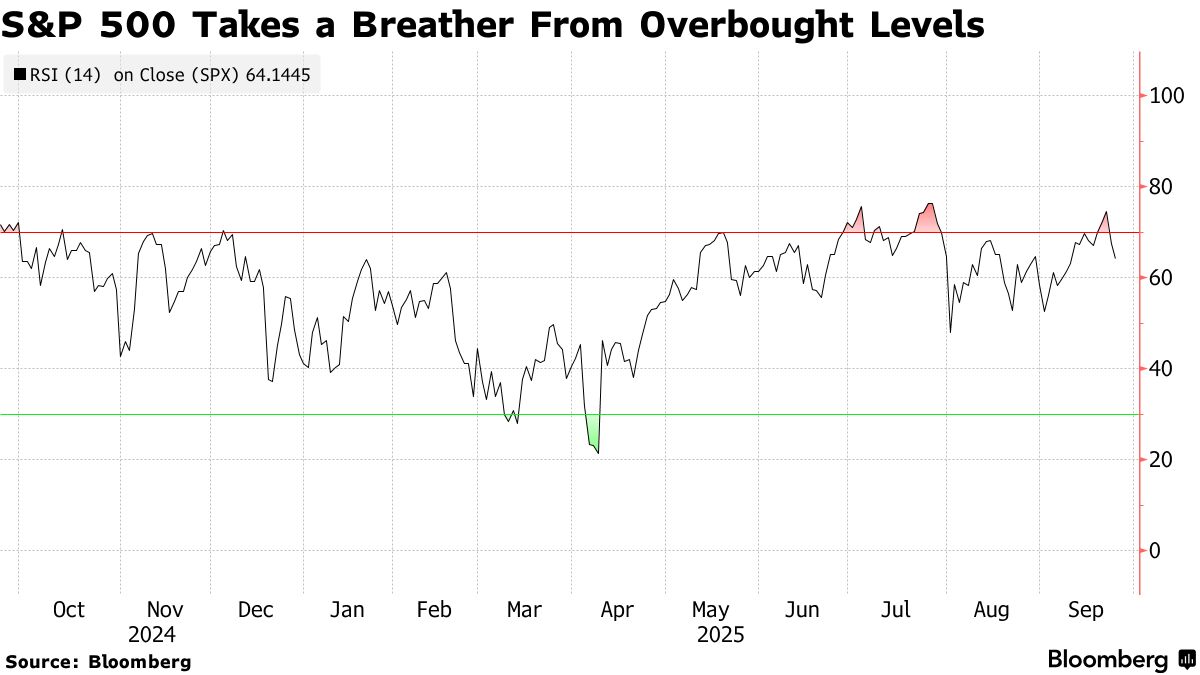

“Timeout called,” said Craig Johnson at Piper Sandler. “The trend of strong gains isn’t over yet. However, the short-term risk-reward profile is becoming more compressed as stocks extend higher while underlying momentum fades.”

The S&P 500 fell 0.3%. Micron Technology Inc., which has almost doubled this year, sank despite an upbeat forecast. Intel Corp. was said to seek an investment from Apple Inc. as part of a comeback bid. Oracle Corp. sold $18 billion investment-grade bonds. Treasury yields and the dollar rose.

Despite the lack of strength on Wednesday, the stock market is holding near its record on the view that the economy is not falling off a cliff and growth will be bolstered by improving corporate profits and the artificial-intelligence boom.

Subramanian at BofA notes that the S&P 500’s multiple may be warranted given better visibility/predictability.

“In theory, investors pay up for predictable assets and are compensated for uncertainty. Perhaps we should anchor to today’s multiples as the ‘new normal’ rather than expecting mean reversion to a bygone era.”

At JPMorgan Chase & Co., Andrew Tyler said “several conversations yesterday focused on what could derail this bullish run. My favorite response was an asteroid hitting the earth.”

Yet after a nearly 35% rally in the S&P 500 from April’s lows, even Federal Reserve Chair Jerome Powell noted this week that equity prices are “fairly highly valued.”

To Mark Hackett at Nationwide, that comment appeared “observational rather than cautionary.” Nonetheless, we could see a period of “consolidation” in the near term.

“That said, sentiment and positioning indicators suggest the rally is underpinned by cautious optimism rather than speculative excess,” Hackett noted. “This positioning and sentiment backdrop supports a constructive outlook for equities.”

The stock market’s sustained push during the traditionally weak seasonal period appears to be fueling “bubble” talk, especially in regard to tech, according to Daniel Skelly, head of Morgan Stanley’s Wealth Management Market Research & Strategy Team.

“While even the strongest rallies inevitably experience retracements, and the market certainly faces ongoing policy and economic uncertainties, there are good reasons to believe this talk is misplaced,” he said.

Over the past 50 years, there have been five bull markets that lasted more than two years, and the average length was eight years. We’re not quite three years into this bull market, which dates back to October 2022, he noted.

This week, the S&P 500’s 12-month forward price-to-earnings ratio touched a high of 22.9, a level that this century was exceeded in just two prior instances: the dot-com bust and the pandemic rally in the summer of 2020 when the Fed reduced interest rates to near zero.

Of course, risks abound, from sticky inflation to the expansion of the US job market moderating.

“The stagflation issue keeps popping its head up every few months,” said Matt Maley at Miller Tabak. Whether Friday’s key price data adds to stagflation fears — or minimizes them — should be important for how the market acts as we move into the month of October, he said.

“We view the Fed’s easing cycle as broadly supportive for equities, quality bonds, and gold, and we continue to recommend a whole-of-portfolio approach when putting cash to work,” said Ulrike Hoffmann-Burchardi at UBS Global Wealth Management.

Ongoing US labor market softness should allow the Fed to cut rates further, she said, adding that her firm sees 25 basis points in cuts at each meeting through January 2026. In her base case, the S&P 500 should trade near 6,800 by June 2026, with a bull case outcome closer to 7,500.

The gauge closed at 6,637.97 Wednesday.

“Even though a digestion of recent gains is always possible, history says (but does not guarantee) that it will be mild,” said Sam Stovall at CFRA. Since World War II, no calendar year that started with a decline of more than 11% went on to have a second slump of greater than 10% within the same year.

“Volatility, on the other hand, should be expected in October, since its standard deviation of monthly returns was 33% higher than the average for the other 11 months of the year,” he said.

Some of the main moves in markets:

Written by: Rita Nazareth @Bloomberg

The post “Wall Street Says ‘Timeout Called’ as Rally Wanes: Markets Wrap” first appeared on Bloomberg

{kind=link}

{kind=link}

{kind=link}