Investment bankers are cheering the recovery in US first-time stock sales. But the revival comes too late to halt a decades-long slump in the number of public companies amid the unchecked growth of private markets.

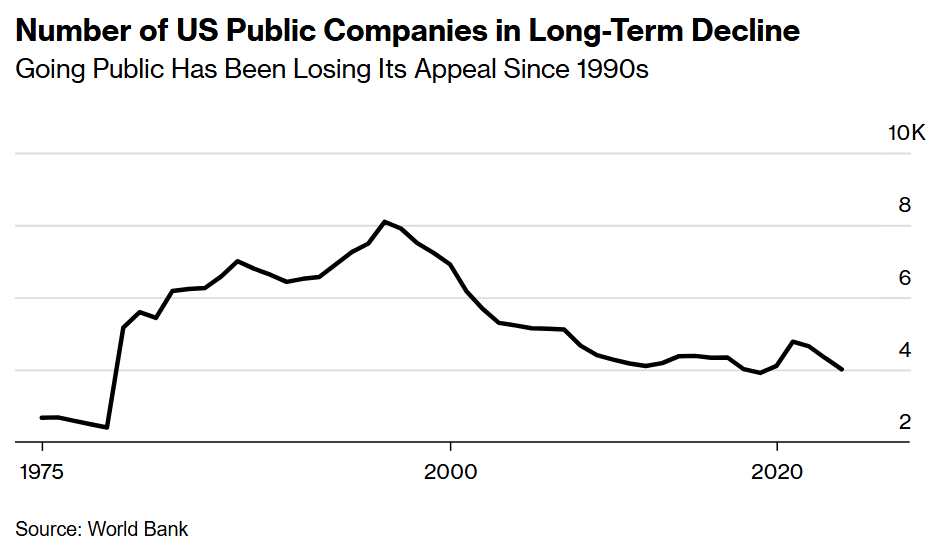

The number of American public companies stood at around 4,000 last year, around half the number there were in 1996, according to a Bloomberg Intelligence report. On the sidelines are nearly 800 closely held US companies valued at more than $1 billion apiece, including three mega-unicorns — SpaceX, Anthropic and OpenAI — each valued at over $100 billion, BI’s report showed.

The uptick in US initial public offering activity this year has raised $32 billion, the most by this point in the year since 2021, according to data compiled by Bloomberg. Still, that represents only about 181 new firms coming to market, barely making a dent in the list of companies that once would have been prime candidates to go public. With the Trump administration opening the door to making private investments eligible for 401(k)s, at this point it’s hard to see what would derail the momentum.

“It’s not only the fact that the federal government has made it so much more difficult to be a public company and so much more expensive, but they’ve also made it a lot easier to be a private company and for these big companies to get bigger through acquisitions,” said Bloomberg Intelligence’s Andrew Silverman.

The rationale for pursing IPOs under the current macroeconomic backdrop might be about more than just raising capital. Since many large firms can raise similar amounts or more outside public markets, part of an IPO’s appeal is mergers and acquisition related, according to Silverman.

IPOs help create acquisition currency, “because they have public, liquid shares which they can tap to acquire companies instead of using cash. That offers more flexibility,” he said. IPOs are more common in M&A-heavy industries and newly public firms are more acquisitive than established ones, according to research cited by BI.

On the other hand, for small and mid-cap companies looking to ultimately sell themselves, going public raises their profile while setting a market price for shares, he added.

An IPO is still the logical destination for many firms, particularly smaller ones, bankers and investors have said. Still, if the situation persists and the ranks of private companies continue to swell, Silverman believes that regulators will be pressured to intervene as these companies lack transparency and could be adding significant risk to the financial system.

Congress and the US Securities and Exchange Commission could eventually act to require these companies to report like public companies or force them to go public when they hit a certain revenue level, Silverman said.

So far the White House has shown little interest in curbing private markets. In August, President Donald Trump ordered federal agencies to make it easier for retirement funds to invest in private companies. The 20 biggest pension funds already have about $550 billion of private market exposure and some have doubled that allocation over the past decade, according to BI.

To Silverman, it might take a financial crisis or major private company collapse endangering retirement assets to catalyze federal action to rein in private markets.

“It would take a concerted effort to change the situation,” Silverman said. “We have so much money in private markets at this point that I don’t know that there’s ever any way to go back again.”

Written by: Anthony Hughes and Yiqin Shen @Bloomberg

The post “US IPO Rebound Does Little to Dent Private Markets’ Rapid Growth” first appeared on Bloomberg

{kind=link}