The foundation is in place for the U.S. and the World’s equities markets to have their worst year since 2008. It’s for three reasons:

2. The war has driven the price of oil to near all-time highs. Oil price peaks since 2008, that have followed the all-time highs for US indices, have coincided with substantial declines for both stocks and oil. Since the war began crude oil has risen by approximately 50%. The conflict, which will levitate inflation and slow economic growth worldwide, has not yet been priced into the markets. The war will also cause the end of the secular bull market for the U.S. which began in 2009. See content about U.S. secular markets below.

3. The war has caused severe damage to the refinery infrastructure of the Middle East. The quote below is from “Qatar Assesses Damage as Energy Strikes Escalate”, Bloomberg 03/19/26.

“The damaged facilities produce about 17% of Qatar’s liquefied natural gas export capacity. It will take three to five years to repair the damage, QatarEnergy CEO Saad al-Kaabi said in an interview with Reuters. The LNG plant had already halted production after a previous drone strike but the subsequent attacks dealt more damage.”

The years that it will take to repair the infrastructure for oil and natural gas facilities will result in a relative increase in the prices for the price of fossil fuels. This will translate into elevated inflation

Based on my research the Iran war will have a duration that is longer than what has been discounted by the markets. The reason why the markets have yet to adjust is because of the optimism that was created from the ease the U.S. had to dispatch Venezuela. An enduring conflict will weigh on US and global investors. A permanent regime change has a low probability of happening even if the U.S. and Israel put boots on the ground. The videos accessible via the link below provide the rationale for why the war will be long and costly. They are clips from the Markowski on the Markets Zoom sessions which are held weekly.

Videos covering why Iran war is very risky for global equities near their all-time highs

https://alphatack.com/videos-covering-why-iran-war-is-very-risky/

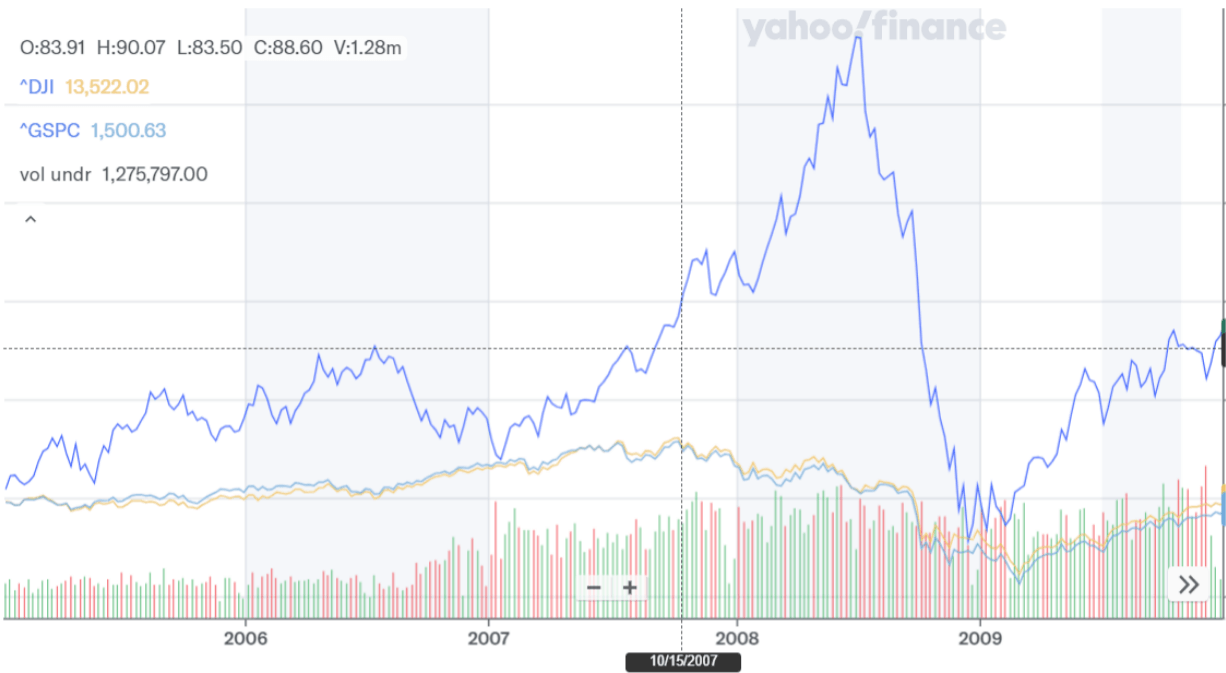

The chart below depicts the price of oil versus the S&P 500 and Dow Jones indices, which reached their all-time highs in October 2007. Oil did not reach its high until 2008 and by March of 2009 the indices and crude had declined substantially.

Chart below depicts crude oil vs. the S&P 500 and Dow Jones indices reached their all-time highs in December 2021. Oil did not reach its high until July of 2022. By November of 2022, the indices and crude had declined substantially.

Both of the 56.4% and the 27.5% declines for the S&P 500 in the above charts were among my crash predictions.

Chart below depicts that the S&P 500 and Dow Jones indices reached their all-time highs in January 2026. Oil began climbing to higher highs in March 2026. Probability for 27% minimum + decline for the indices from their all-time highs is very high.

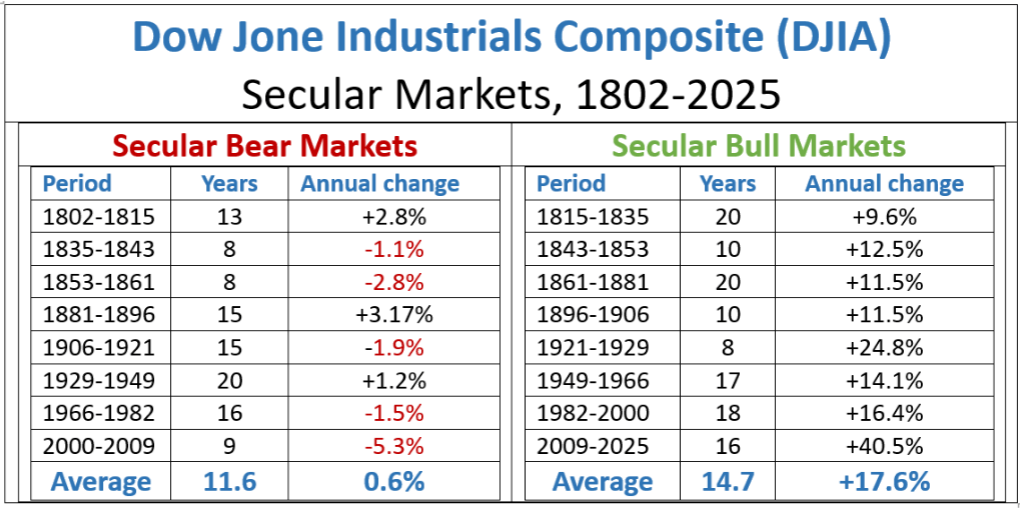

The Dow Jones and S&P 500 indices made relatively quick recoveries back to their all-time highs after their 2020, 2022 and 2025 double digit declines. The probability of the quick recoveries after the coming crash is low. Its because both of the indices have had secular patterns since their inceptions. The table below contains the secular markets for the Dow which is the oldest US index. Secular is defined as minimum/maximum up and down periods of eight to 20 years. Since the very beginning secular bulls have been followed by secular bears. The existing bull, which began in 2009, is now In its 17th year. Since its long in the tooth the probability for it to recover and continue on is slim. This is especially due to AI powering the Dow to an iconic bubble high. The average annual return during secular bulls has been 17.6%. The return for a secular bear has been 0.6%.

The problem for the secular bears is that they are extremely volatile. The chart below depicts that if one had bought and held the Dow from 1920 to 2025, the gain was 2,93%. However, secular bear declines ranging from 49% to 89% occurred.

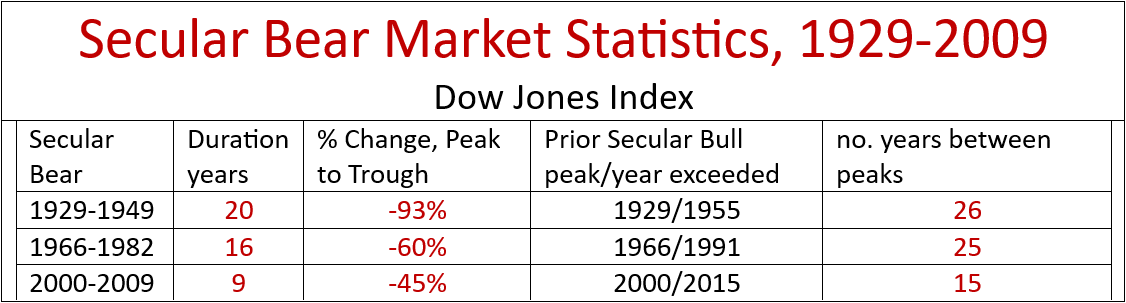

The table depicts the number of years required for the Dow to get back to its prior secular bull high. Based on the statistics should the Dow enter into a secular bear market in 2026 , the 2026 all-time high would not be surpassed until as early as 2041 and possibly by as late as 2052.

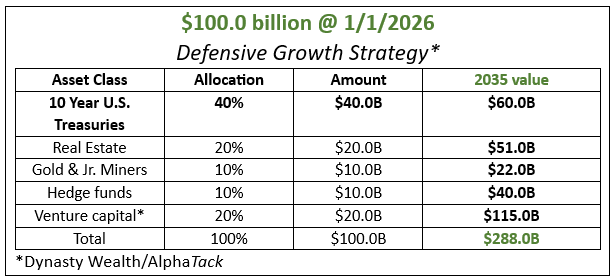

My recommendation is for all investors to liquidate their publicly traded holdings including mutual funds. The proceeds can be utilized to deploy my defensive growth strategy (DGS). The table below contains the allocations for the strategy.

A video that covers secular markets and the DGS in the above table and also the defensive strategy that Stanley Druckenmiller is recommending is below. Mr. Druckenmiller, who is among the world’s top hedge fund managers, is predicting a significant decline for the U.S. indices to begin in 2026. His rationale for the decline, which is different than mine, is covered in the video.

Michael Markowski, Director of Research for AlphaTack.com. Developer of “Defensive Growth Strategy”. Entered markets with Merrill Lynch in 1977. Named “Top 50 Investor” by Fortune Magazine. Formerly, underwriter of venture stage IPOs, including one acquired by United Health Care for 1700% gain. Since 2002 has conducted empirical research to develop algorithms which predict the negative and positive extremes for the market and stocks. Has verifiable track records for predicting (1) bankruptcies of blue chips, (2) market crashes and (3) stocks multiplying by 10X. In a 2007 Equities Magazine article predicted the epic collapses for Lehman, Bear Stearns and Merrill Lynch. Most recent algorithm developed from research of UBER and AirBnB has enabled identification of startups having 100X upside potential within 7 to 10 years.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}