Property mogul Barry Sternlicht last week said there’s $1.2 trillion of real estate losses in offices alone and “nobody knows exactly where it all is.” Investors are growing alarmed that smaller banks might be on the hook for much of the wipeout.

Concerns mounted over the past two weeks after New York Community Bancorp, under pressure from a US watchdog, slashed its dividend to help stockpile funds in case commercial real estate loans go bad. And property values may have room to fall further, only adding to the pain for lenders: research firm Green Street estimated this week that appraised values of properties may need to drop another 10% to reach fair valuations.

The turmoil is a blow for landlords and bankers who were waiting for lower borrowing costs to ease the pain, embracing the mantra of ‘Survive Til ‘25.’ While that looked a good bet a couple of months ago, the robustness of the economy may cause the Federal Reserve to cut rates at a slower pace than markets had expected, increasing the risk of write downs at smaller lenders after they pushed into commercial real estate lending in recent years.

Equity investors have been selling off regional bank shares since the NYCB surprise, but credit investors seem more sanguine, suggesting they see the issues as an earnings issue rather than a financial stability risk. In fact, risk premiums on bank bonds are narrowing more than the broader market, signaling banks bonds are performing better.

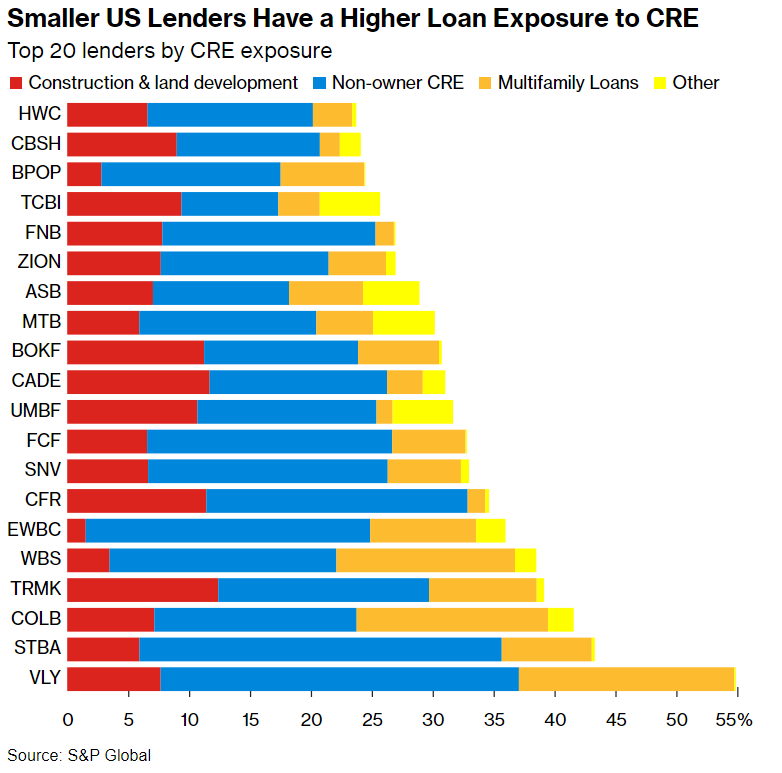

That said, CRE credit makes up more than 40% of some lenders’ loan books and the Fed is working with community and regional banks with concentrated exposures to commercial property. That includes coming up with a plan to work through expected losses, chairman Jerome Powell said in an interview with CBS’s 60 Minutes that aired Sunday evening.

One reason for that is higher capital charges made CRE loans less attractive to the largest banks after the financial crisis. Smaller lenders that faced fewer capital requirements saw a chance to boost market share and piled in, increasing their exposure just as interest rates began to rise.

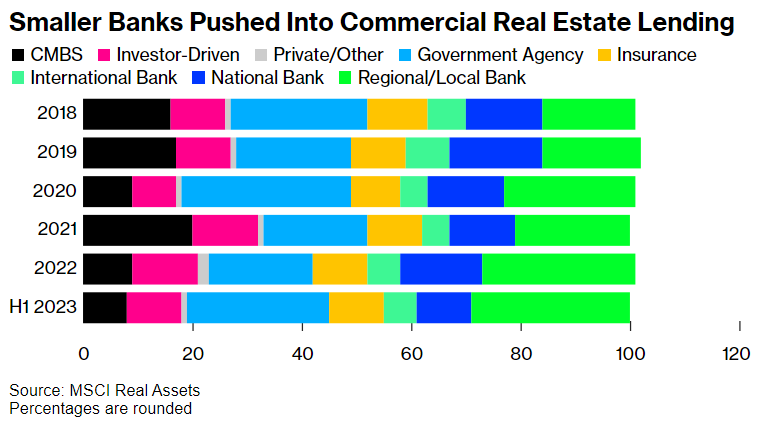

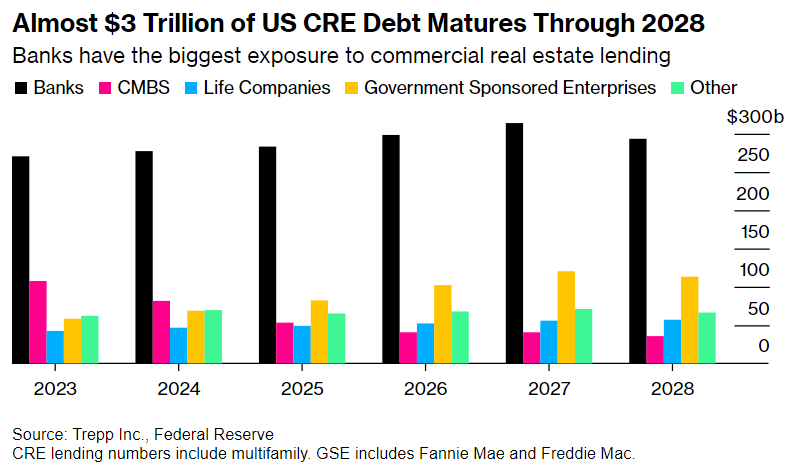

The upshot now is that banks are by far the largest source of finance to the industry. With many of them hamstrung by losses, it will be harder for borrowers to refinance, increasing the risk of losses.

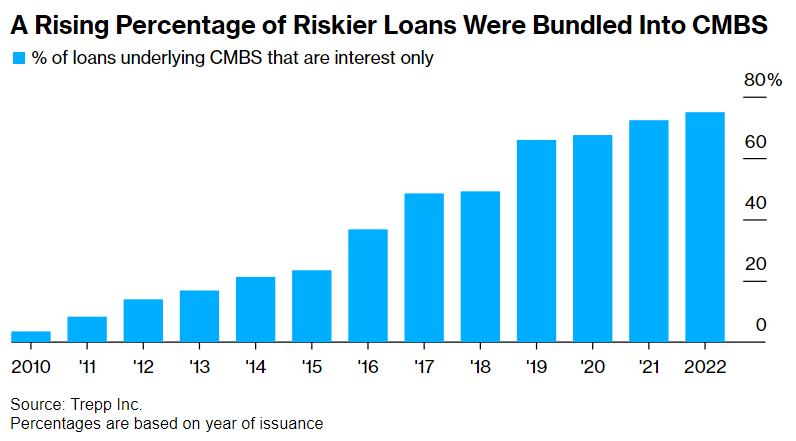

An additional complicating factor for lenders in the US is the amount of CRE lending that was interest-only, at least for mortgages bundled into bonds. While loan-to-value ratios may have been conservative, the decline in property values there has been so large it’s left bondholders vulnerable to losses in their commercial mortgage backed securities portfolios.

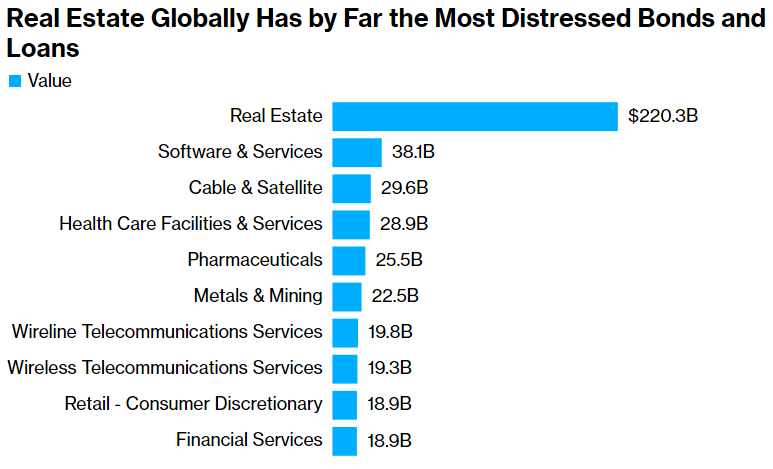

The troubles with CRE are by no means limited to the US. Real estate is the industry accounting for the largest amount by far of distressed bonds and loans globally, much of it from China which has been in a property downturn for more than three years. Distress has also spread to Germany and the Nordic nations, after a splurge using cheap borrowing turned bad as borrowing costs rose.

More than $220 billion of bonds and loans linked to property are currently distressed globally, according to data compiled by Bloomberg News. That’s a fall of just $11.4 billion since Powell said in mid-December that the interest-rate hiking cycle was essentially over and that discussion of possible cuts was coming “into view,” sparking a rally in a wide array of securities markets.

About $30 billion of US high-grade bond sales are expected next week.

In Europe, 75% of professionals surveyed expect over €30 billion ($32.4 billion) of sales in the coming week.

In the US, January headline and core CPI — due Feb. 13 — both likely rose 0.2%, moderating from 0.3% prior. January retail sales, due Feb. 15, are expected to show a modest month-over-month gain of 0.2%.

The UK will release its jobs data on Feb. 13.

UK’s January CPI data, to be released on Feb. 14, is forecast to show 4.1% year on year, up from 4% in December.

In the UK’s fourth quarter 2023 GDP print, due Feb. 15, output is expected to post a second consecutive quarterly drop of 0.1%, meeting the definition of a technical recession, which will likely last until early 2024.

For an in-depth look at the data and events around the world that could impact markets in the coming week, see the Global Economy Week Ahead from Bloomberg Economics.

Written by: Neil Callanan @Bloomberg

The post “These Six Charts Explain How the CRE Debt Crisis Spread to Banks” first appeared on Bloomberg

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}