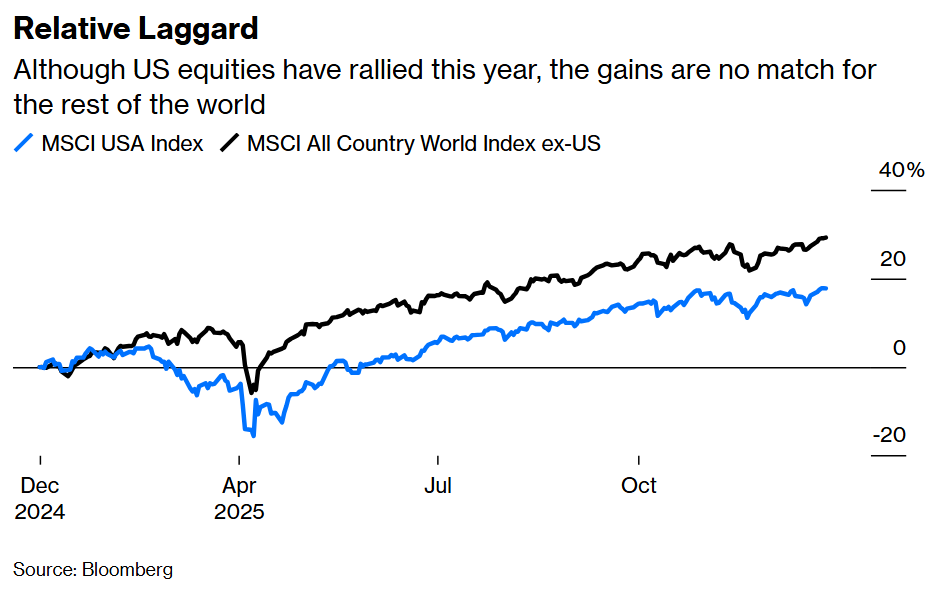

It’s the time of year when investors peek at their accounts to see whether it will be champagne and caviar to celebrate the holidays or beer and chips. The MSCI USA Index’s 16.3% gain would suggest the former is on the menu, and yet, the latter might be more appropriate.

Yes, stock gains have comfortably exceeded the long-term average for a third straight year. But the result hardly ratifies President Donald Trump’s oft repeated assertion that the US is the world’s “hottest” country. Stacked up against the rest of the world, America’s stock market looks like an also ran: The MSCI USA’s advance pales next to the 29.2% surge in the MSCI All Country World Index excluding America.

To understand just how poor this performance was, consider that nothing of this magnitude has happened since 2009, when the global economy began to recover from the financial crisis. Stocks are no anomaly, US bonds and the dollar are relative losers as well.

The best explanation for why investors discounted US assets so soon after The Economist dubbed the American economy “the envy of the world” can be found in the latest OECD forecasts. Coming into 2025, the Paris-based organization predicted the US economy would grow 2.4% for the year, trouncing the rest of the developed world’s 1.9%. Now, the OECD predicts a less optimistic 2%. It sees a further downshift in 2026, to 1.7%, matching the OECD overall.

It’s a similar story with inflation. As 2024 wrapped up under the Biden administration, the OECD figured price increases were under control, projecting a 2.1% rate of increase in 2025. Now, it calculates consumer prices likely rose 2.7% and will reach 3% in 2026.

In other words, America’s economic premium has vanished. It’s not hard to understand why. Whether it be tariffs, foreign policy, healthcare, immigration, national security, energy, education or, quite frankly, any issue that impacts both businesses and households, the Trump administration has trafficked in chaos. Perhaps it was shortsighted to elect a “businessman” whose campaign centered around inflicting retribution on those he felt wronged him, both domestically and internationally, and who put a tax on imports and consumption at the heart of his economic agenda.

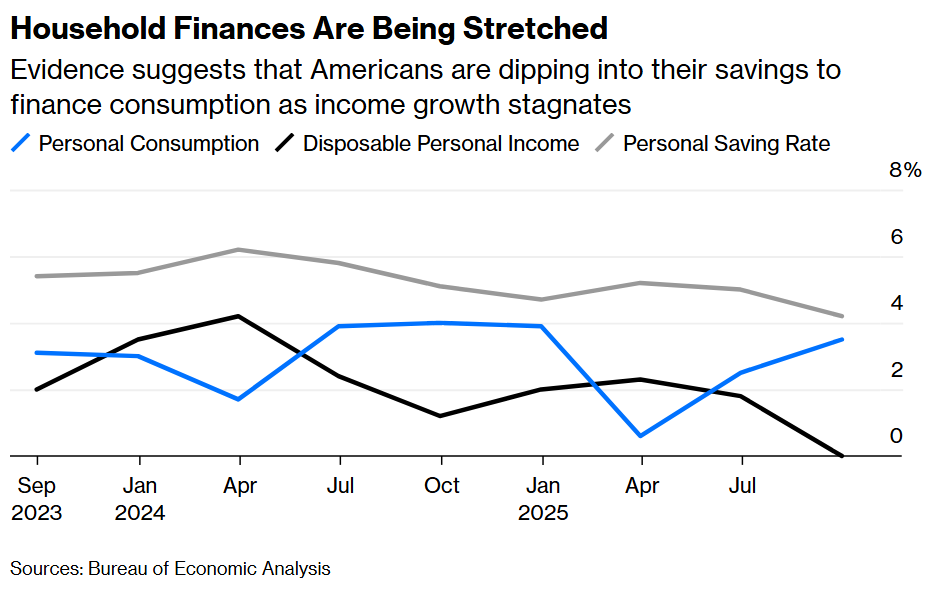

But what about the third-quarter gross domestic product report, which showed the economy expanded at a 4.3% annual rate, exceeding the median estimate of economists? Consider the troubling internals. The gain was powered by a 3.5% surge in personal consumption, while real disposable incomes were flat. Such a divergence suggests households are digging into their savings to make ends meet. It can’t last. In fact, the personal saving rate has dropped to 4%, the lowest since 2022, when inflation was raging.

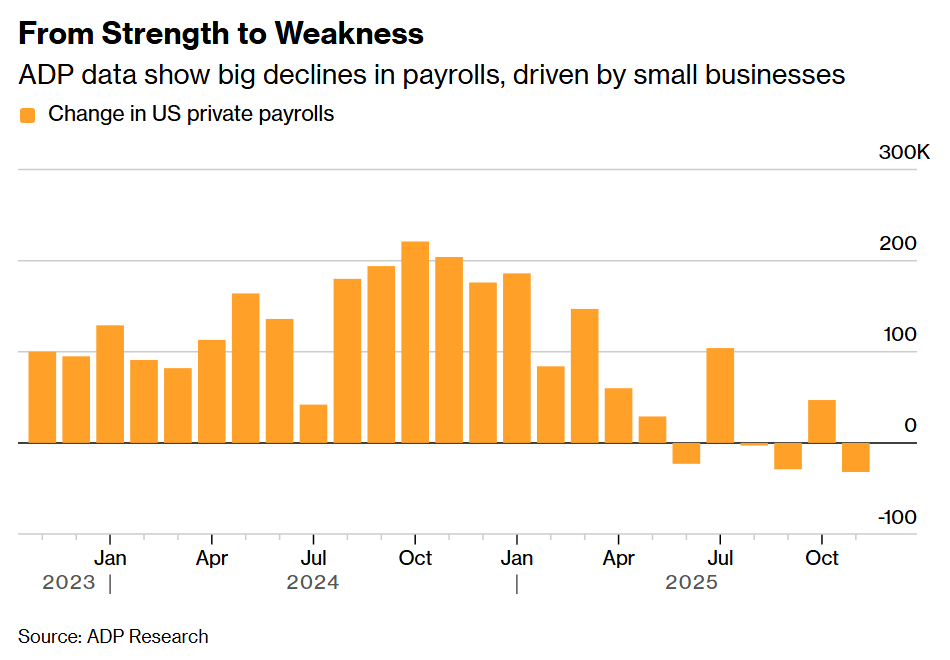

For companies, it’s almost impossible to plan when policy is so unpredictable. The latest survey of the nation’s chief financial officers by Duke University and the Federal Reserve Bank of Richmond shows optimism about the economy is no different than in early 2020, when the global pandemic was raging and everyone was worried about a depression. Small businesses drive job growth. The problem is that private employers in both goods- and services-producing industries are slashing workers, according to the November ADP National Employment Report. Businesses with fewer than 50 employees cut 120,000 jobs, the largest one-month decline since May 2020.

Although earnings by public companies are strong and rising, that’s not the case for most other businesses. The latest official profits data published in the national income and products accounts suggests a 5.6% contraction in earnings in the year through June, according to JPMorgan Chase & Co.

“There is just not much going on right now, and we believe it’s all tied to the chaos and uncertainty coming from Washington,” is how one respondent put it in the Federal Reserve Bank of Dallas’s monthly manufacturing survey. Indeed, the Washington Post reports that at least 717 companies filed for bankruptcy in 2025 through November, based on data from S&P Global Market Intelligence, the most since 2010.

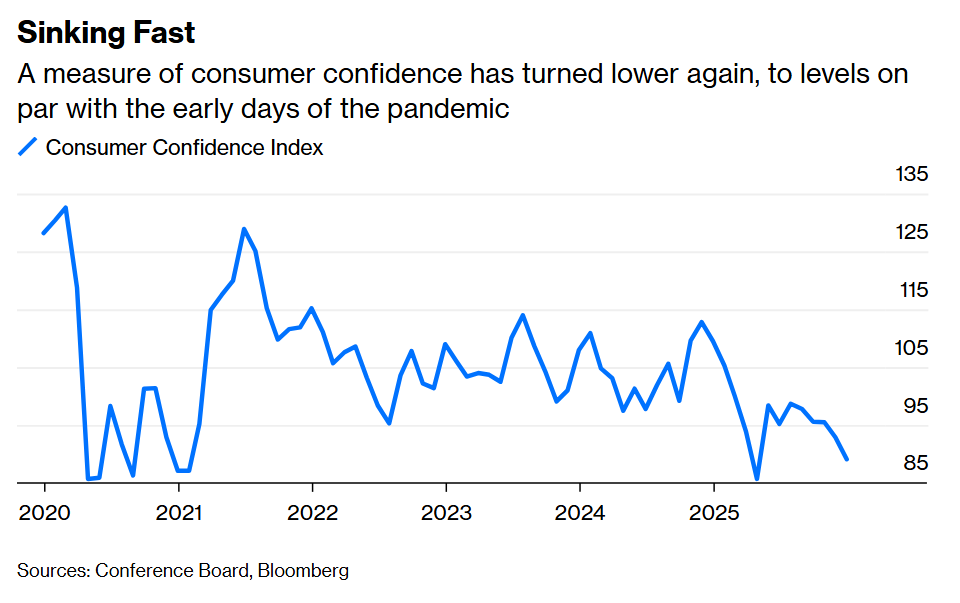

No wonder households are worried. The Conference Board’s measure of consumer confidence has dropped to levels on par with the first few months when Covid-19 was ravaging the world. “Consumers’ write-in responses pertaining to factors affecting the economy continued to be led by references to prices and inflation, tariffs and trade, and politics, with increased mentions of the federal government shutdown,” Dana Peterson, chief economist at the Conference Board, said in a statement accompanying the November results.

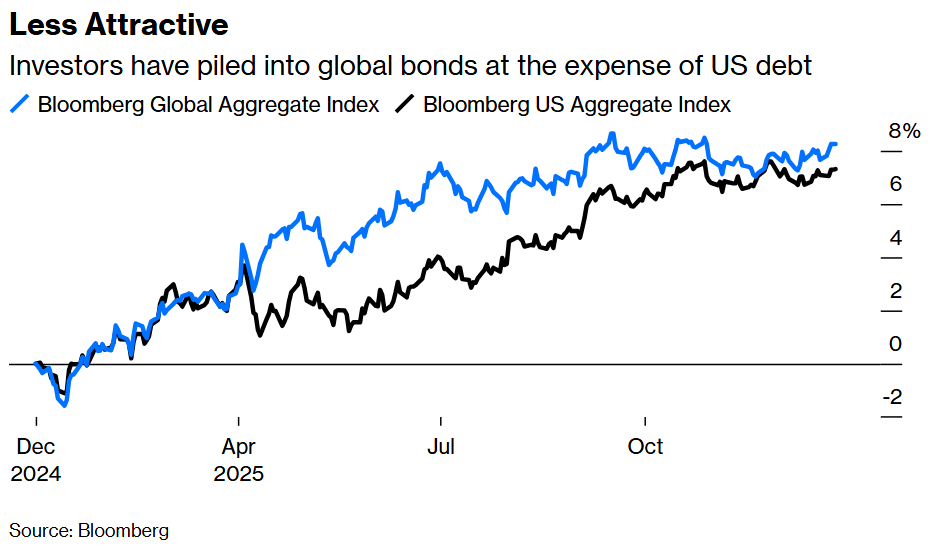

In the bond market, returns from US fixed-income assets trailed the world overall. Despite the Federal Reserve cutting benchmark interest rates three times since mid-September, investors took the unusual step of pushing long-term yields higher amid jitters over a possible reacceleration in inflation . As a result, the Bloomberg US Aggregate Index rose 7.30% in 2025, lagging behind the Bloomberg Global Aggregate Index’s gain of 8.17%.

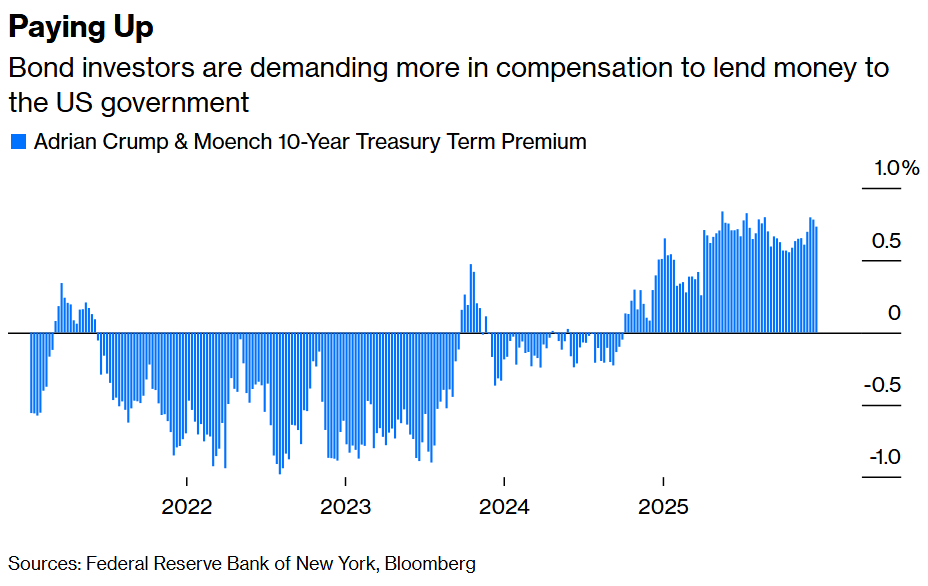

A look under the hood reveals some disturbing trends. For one, there’s ample evidence that borrowers are demanding more than is typical to lend longer term to the US government. One such measure is the term premium on the 10-year Treasury note, which is essentially the extra compensation investors demand to own long-term bonds rather than buying and continually rolling over short-maturity securities such as Treasury bills. It surged to 0.91 percentage point in the weeks after Trump’s disastrous “Liberation Day” tariff announcement in April, the most since 2014, and has remained elevated.

This comes amid evidence that foreign official accounts, such as central banks and sovereign wealth funds are diversifying away from America’s government debt. “Official” holdings of US Treasuries fell by $25 billion in October and have declined by $46 billion for the year through October after dropping by $27 billion in all of 2024. Official holdings are now down to about 13% of US marketable Treasury securities from about 33% a decade ago and almost 40% 15 years ago. A smaller pool of lenders to America would generally lead to higher interest rates than otherwise not just for Washington, but for businesses and households, too.

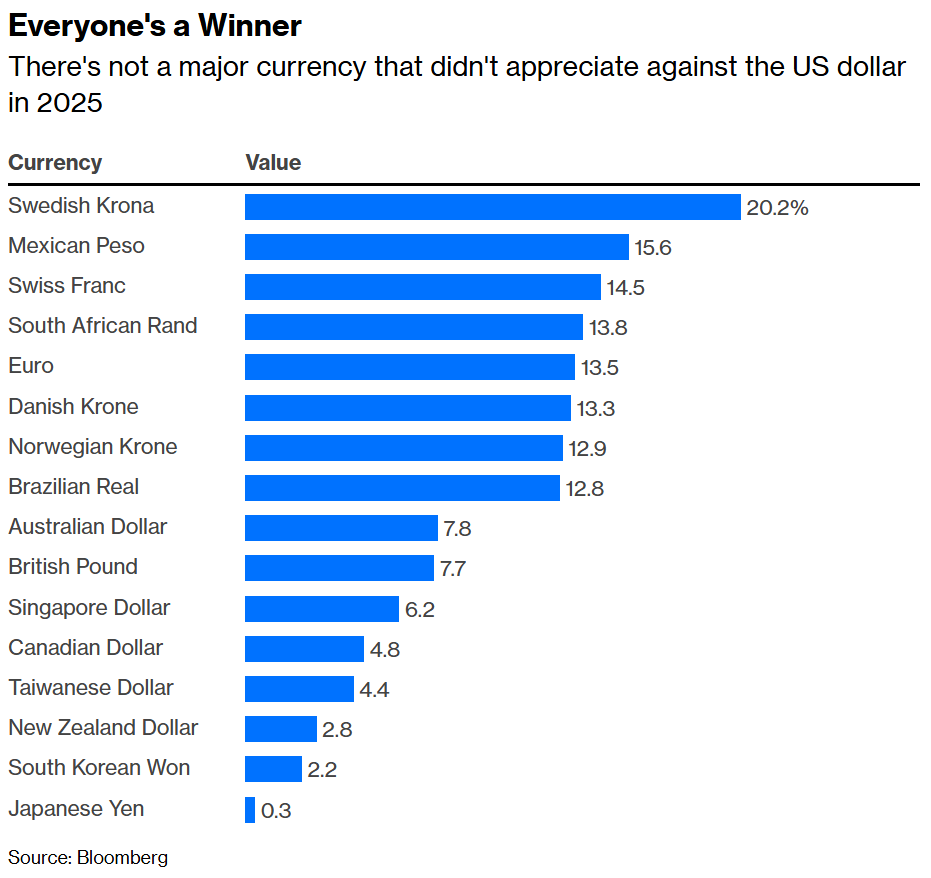

A nation’s currency is not much different than a company’s share price in that it’s probably the best indicator of sentiment. If so, the US is in trouble. The Bloomberg Dollar Spot Index, which measures the currency against its major market peers, fell about 8%, the worst showing since 2017 — the first year of Trump’s first term. The greenback depreciated against all the world’s 16 most-traded currencies as tracked by Bloomberg, a clear sign that investors are pushing back against Trump administration policies.

A weaker currency makes exports more competitive, but it adds to inflation by making imports relatively more expensive. So while exports for the year through September are up 4.7% to $1.62 trillion, imports are up 7.4% to $2.60 trillion, according to the Bureau of Economic analysis.

The sad thing is that the Trump administration knows the detrimental effects of its policies, with top officials including Treasury Secretary Scott Bessent and Commerce Secretary Howard Lutnick repeatedly pushing back the timing of when the economy will flourish, from definitely in 2025 to sometime in 2026. Rather than a new “Golden Age,” it increasingly looks as though Americans were sold “Fool’s Gold.”

Written by: Robert Burgess @Bloomberg

The post “The Year America’s Economic Edge Evaporated” first appeared on Bloomberg

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}