{kind=link}

{kind=link}

{kind=link}

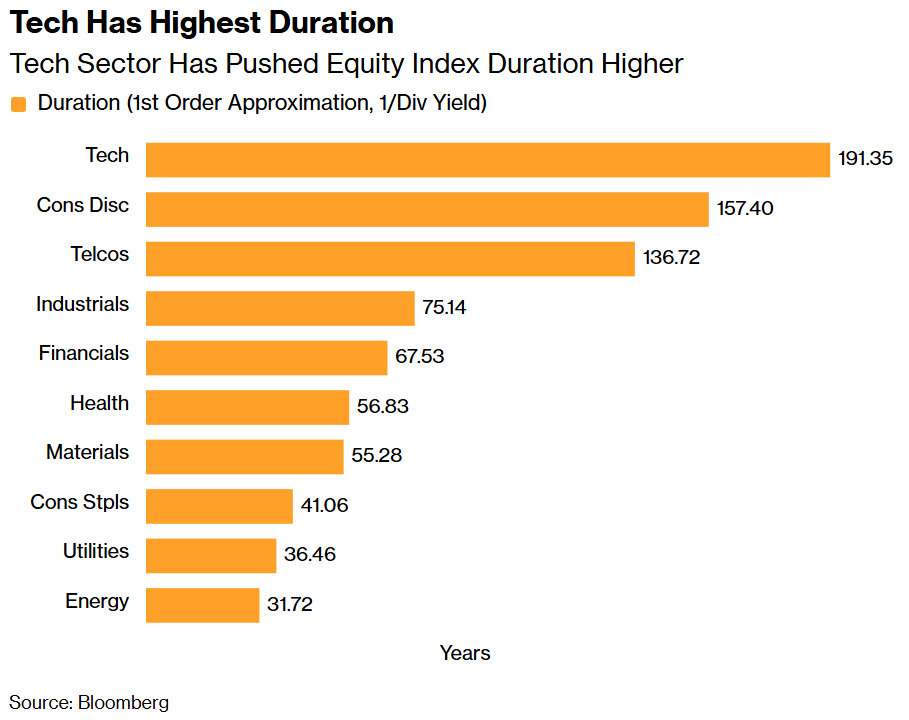

Tech has the largest duration, followed by consumer discretionary and telcos, while utilities and energy have the lowest duration.

All through this decade, investors have been adding to their duration exposure, if we look at the steady and almost uninterrupted ascent of duration-weighted flows into sector ETFs.

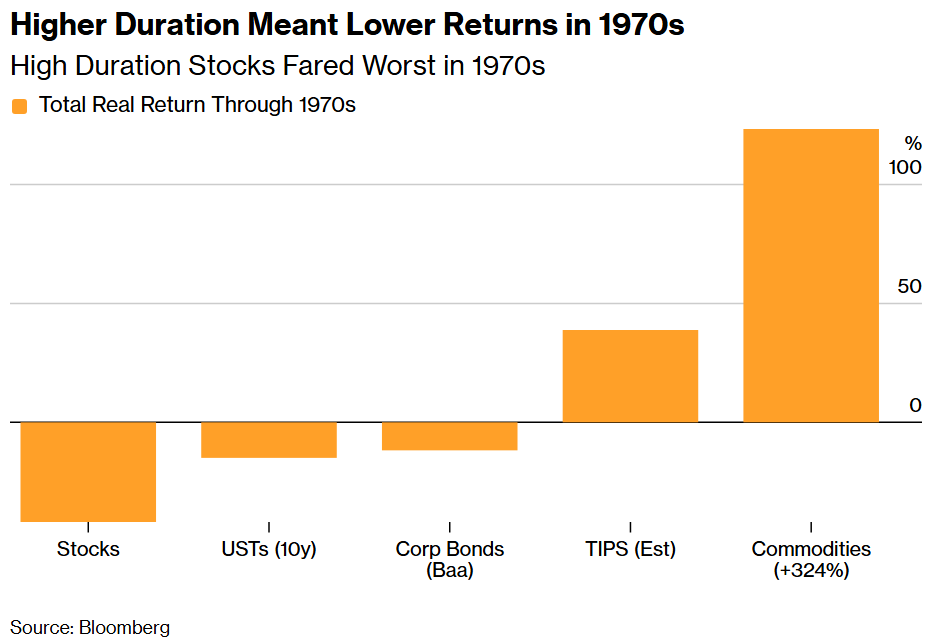

But that is now a glaring vulnerability for the market. An overbought market and its most overbought sector are laden with duration when we are coming into a period of renewed inflation, as anticipated by a surfeit of leading indicators.

The hope among tech bulls is that the productivity revolution unleashed by AI will also neuter price pressures. But that relies on disinflation arriving at the same time as the inflation, and that job losses won’t lead to a further rise in a fiscal deficit that is already very conducive to higher prices.

It’s possible the belief that stocks are a good inflation hedge could carry them some way. But it won’t take long for fundamentals to catch up as investors remember why owning duration when there’s inflation is a very bad idea.

The MacroScope column is a wide-angled take on the most important macro and market topics, rising above the short-term noise to get the big picture

Simon White is a macro strategist who writes for Bloomberg. The observations he makes are his own and not intended as investment advice.