Investors are piling in to exchange-traded products, betting that stock-market volatility will increase from rock-bottom levels. But while they wait to cash in on a big spike, their returns are dwindling due to a quirk of the market.

The largest product that follows the performance of Cboe Volatility Index futures, the Barclays iPath S&P 500 VIX Short-Term Futures ETN, has increased assets by more than 300% this year to over $1 billion. The attraction is that if the record stock rally withers, market volatility will spike, delivering spectacular returns.

But these securities contain a trap for investors who hold them for too long: They burn through cash when traders think market swings will be greater in the future than now. And the more assets that flow into these products, the more gruesome these carry costs become.

Bloomberg Intelligence’s senior ETF analyst Eric Balchunas compares VIX ETPs to a “chainsaw” — very effective at certain jobs, “but it can cut your arm off.”

These products promise specular returns in the event of a spike in the VIX. Time it right, and you can win big. Anyone who bought the Volatility Shares 2x Long VIX Futures ETF on April 1, just before sweeping US tariffs were imposed, would have tripled their money if they sold a week later on April 8.

But to realize those returns they would need to get in and out at just the right moment. If investors held that same fund for the past year, they would be down 78%, according to data compiled by Bloomberg.

| Ticker | Returns Since Sept. 26 2024 | Total Assets (Millions) | Net Fund Flows Over 1 Year |

|---|---|---|---|

| VXX | -32% | $1,000 | 312% |

| UVIX | -78% | $510 | 215% |

| UVXY | -57% | $690 | 150% |

| VIXY | -33% | $343 | 115% |

“These can increase in price pretty dramatically, almost like an option” but without an expiration date, said Michael Thompson, co-portfolio manager at Little Harbor Advisors. “So if your anticipated correction or drawdown in that broad equity market doesn’t happen by a particular date like you need for an option, you can still hold on to your long vol ETP shares.”

These offer a simple hedging tool for long-only investors, given the propensity for the volatility gauge to jump when the S&P 500 Index sells off. And unlike in 2018, when the flood of speculative investment into short VIX products sparked a spike in volatility known as “Volmageddon,” this influx of hedging isn’t expected to cause a market upset.

Retail traders are “looking to do something cautious, something protective,” said Rocky Fishman, founder of the research firm Asym 500. Fishman estimates that around 40% of the open interest in VIX futures is now owned by VIX exchange-traded products.

The costs of holding these instruments are substantial. Take UVIX: It has a headline expense ratio of 2.8%, and right now the ETF holds two VIX futures, expiring in October and November. Each day, the fund sells some October contracts and buys November, until October expires and the November position starts to be gradually shifted to December, and so on.

With October trading below November, the fund sells low, buys high — bleeding away money. On top of that, the act of rolling the contracts further depresses the value of the front-month future and boosts the next-month bet.

“They have to sell the front one and buy the second one on a daily basis to keep their expiration at a weighted 30 days,” said Michael’s brother and co-portfolio manager Matthew Thompson. “It stands to reason that the front two months should steepen, which, ironically, increases the carrying cost of those instruments.”

These aren’t the first ETPs to run into the roll issue. More than a decade ago, retail investors seeking to mimic gains in oil prices poured money into the United States Oil Fund ETF, only to see their returns lag far behind crude spot advances.

Implied volatility — the market’s best guess as to how much prices will swing in the future — has been largely restrained as stocks grind higher. The main reason for that has been small realized market moves — traders won’t pay up for an option betting on a move, when recent history signals it’s unlikely to happen.

That’s been especially pronounced for immediate volatility, with the S&P 500 trading in tight ranges. This has kept short-term options implied volatility cheaper, which in turn depresses the spot VIX index and front-month futures.

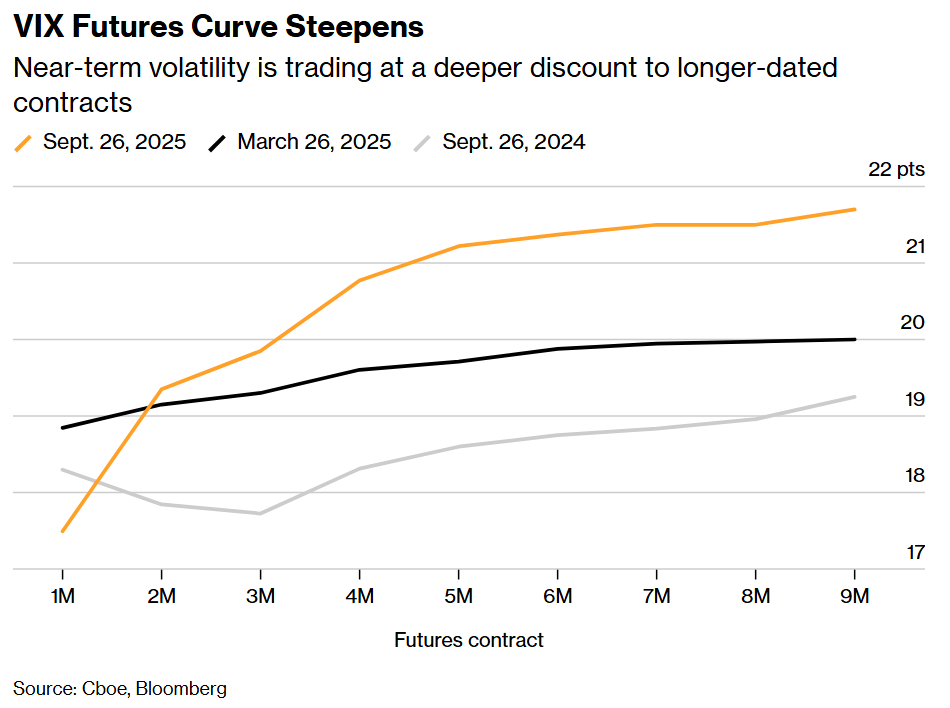

Strategists at Societe Generale SA suggested strategies to take advantage of the steep discount — or contango — in the futures curve. In a Thursday report, they noted it’s not just in contango, but also concave — so the closer to expiration, the steeper the slope.

The trades are variations on shorting the front of the VIX curve. One example is selling the near-term future and buying the next month, as the front-month tends to sink more than the second month as it nears expiration.

The trade has perils, of course. The strategists, including Brian Fleming and Kunal Thakkar, highlighted “the main risk is a sharp and volatile equity selloff, which manifests itself through the VIX curve moving upwards and inverting significantly.”

Investors looking for a hedge against potential losses in their portfolios from a stock selloff may not care about the bleed as much as retail investors. That’s likely to continue boosting inflows into the funds.

Plus hedge funds use them as well, especially for short-term trading, according to Robert Harlow, associate head of global multi-asset research at T. Rowe Price Group Inc.

“If you’re a macro hedge fund that isn’t set up to trade all types of option structures or something, you just get in, get out.”

Written by: Bernard Goyder — With assistance from Elena Popina @Bloomberg

The post “Investors Pile Into Funds Betting on Elusive Market Volatility” first appeared on Bloomberg

{kind=link}

{kind=link}

{kind=link}

{kind=link}