Market jitters over trade could damage more than your retirement fund balance. When investors feel less wealthy, they may also choose to spend less.

Income is a paycheck, but wealth is at least partially a vibe. One day a portfolio of stocks is worth $100,000, and the next it might be worth $98,000 or $102,000, depending on the mood of the traders. When fluctuations in paper values are enough to make consumers feel richer or poorer and change their spending habits, it’s known as the wealth effect.

It’s often said that Wall Street is different from Main Street, but the wealth effect is a link between the two. That connection is on a lot of people’s minds now as fears about President Donald Trump’s sweeping but ever-changing tariff plans roil stock markets around the world. This month the S&P 500 has touched bear-market territory—a sharp comedown after two straight years of gains above 20%. Investors’ faith in the so-called Trump put, the widely held notion that this president will always change course to avoid the pain of a falling market, is being tested. Implicitly, many traders had assumed that Trump himself was a big believer in the wealth effect.

Could market gyrations actually make the real economy worse? Mark Zandi, chief economist at Moody’s Analytics, estimates that last year the booming positive wealth effect added a full percentage point to consumer spending growth, which in turn increased gross domestic product by about 0.5%. Now he’s concerned about a reversal. On the way down, Zandi calculates that for every $1 decrease in household net worth, consumer spending could decrease by 2¢ via the negative wealth effect.

The wealth effect is both psychological and practical. People may choose to spend less as they see the balances in their brokerage accounts or 401(k) workplace saving plans drift lower. Or in the hope of a market recovery, they may decide to wait before they liquidate assets to fund big-ticket spending. “They’re going to be more circumspect about expenditures, about that extra vacation,” says Yung-Yu Ma, chief investment officer at BMO Wealth Management.

There are also some squishy factors that are harder to precisely measure. A Visa Business and Economic Insights analysis notes that there’s been an explosion of financial news made available instantly on smartphones—not to mention on popular free trading apps. That means people are able to get stock market news anywhere and anytime, including when they’re shopping at Target and deciding whether to splurge a bit. Stock market performance is highly correlated with consumer sentiment: People might just be reading the latest market news as a temperature check on the future health of the economy.

Of course, it’s tricky to unravel cause and effect. The stock market might simply rise or fall for the same reason spending does—because investors and consumers share a feeling about the economy. (Consumer sentiment was sliding this year before the April stock rout.) There are also countervailing forces. In a review of the evidence for the wealth effect, economists Daniel Cooper and Karen Dynan note that high returns may encourage people to stuff more money into investments.

A study in American Economic Review: Insights sheds light on the subject by tracking how sudden market gains affected individuals over a longer period. The researchers found that investors responded to windfalls by adjusting spending by a small amount immediately and then continued to spend more over time. Wealth itself really matters.

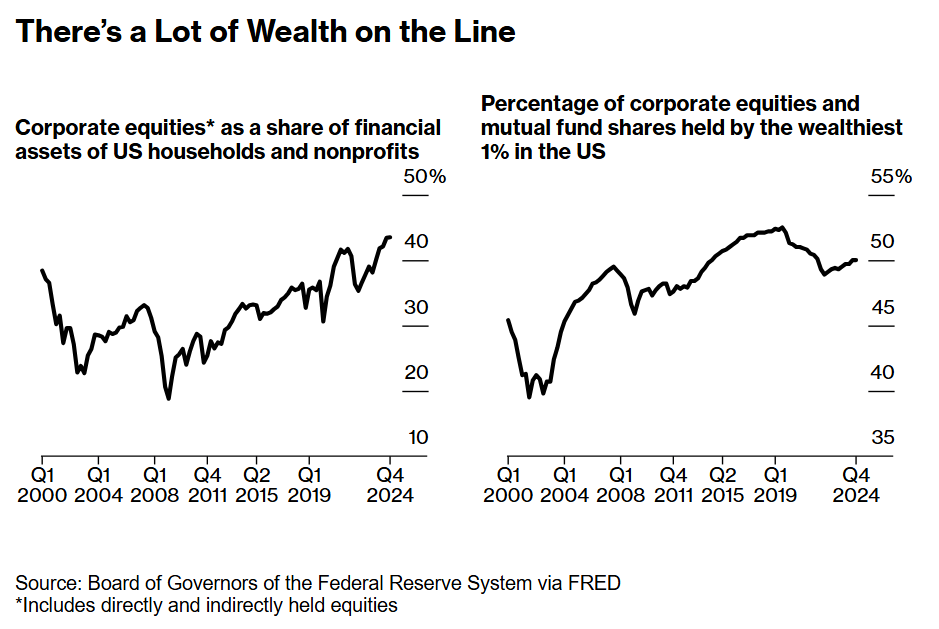

Americans have a lot of money in stocks. According to Gallup, about 62% of households own stocks either directly or through a fund. In the fourth quarter of 2024, households allocated almost 43% of financial assets to equities—a record. In the European Union, the comparable figure was 36% for 2023; in Japan, it was less than 20% last year.

The richest 1% in the US held roughly half the total value of corporate equity and mutual funds, Federal Reserve Bank of St. Louis data show. The 90th to 99th percentile own around 37%. That means equity wealth is hardly the only measure of a healthy economy. But the affluent are an important force in spending. Moody’s Analytics has found that the richest 10% of American households make up almost half of consumer spending now. It was closer to 40% in the 1990s.

The middle class can be exquisitely sensitive to markets too. With the decline of traditional pensions, a record $15 trillion is held in individual retirement accounts, notes Yardeni Research. And half of 401(k) plan participants age 55 to 64 in a Vanguard survey had balances of at least $87,500; the average was more than $240,000. Much of that is in stocks.

Roughly two-thirds of families in the US own homes, according to 2020 estimates by the JPMorganChase Institute. Baby boomers, the wealthiest generation, are sitting on a lot of built-up equity. About 40% of them have lived in the property they own for at least 20 years, according to real estate brokerage Redfin. There are also millions of homeowners who snapped up mortgages at historic low rates of 3% or even less. That’s helped keep home values high—people are reluctant to sell—and left many owners with lots of leftover income to spend. A sturdy housing market could help offset a stock market shock.

But home values cut both ways. What’s wealth for owners is a cost for renters. A 2023 paper found that increases in house prices made owners more likely to spend but renters less likely to. The effect was stronger on renters who were hoping to buy.

The rise of speculative investments, especially among younger households, adds to the complexity of the wealth effect. Crypto produces sudden lotterylike gains and sharp losses. That probably matters a lot to Lamborghini dealers. One group of researchers found that every dollar of unrealized crypto gains stimulated 9¢ of spending, far higher than the effect of stock gains. Crypto also had a noticeable effect on some housing markets.

Even with recent spasms in the stock markets, valuations of all kinds of assets are high. Huge amounts of money have been bet on the so-called Magnificent Seven tech companies and artificial-intelligence-related stocks. Wealth has been elevated over the past decade by unusual investor optimism. No wonder everyone is on edge about a shift in the market’s emotional weather.

Written by: Isabelle Lee @Bloomberg

The post “How Stock Market ‘Wealth Effect’ Could Slow the Economy” first appeared on Bloomberg

{kind=link}

{kind=link}