Moody’s Ratings cut France’s credit outlook to negative from stable, adding to warnings on the country’s bloated public finances as a weakened minority government struggles to pass a budget.

“The decision to change the outlook to negative reflects the increased risk that the fragmentation of the country’s political landscape will continue to impair the functioning of France’s legislative institutions,” the firm said in a statement on Friday. “This political instability risks hampering the government’s ability to address key policy challenges such as an elevated fiscal deficit, rising debt burden, and durable increase in borrowing costs.”

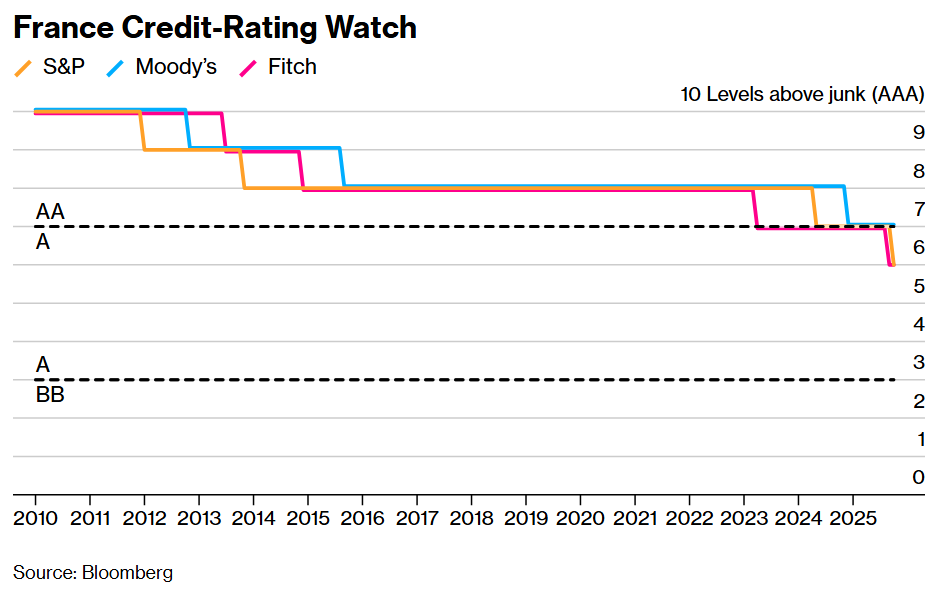

France’s rating at Moody’s remains seven notches above junk at Aa3, on par with the UK and Czech Republic.

France has suffered a string of ratings setbacks in recent weeks including downgrades from S&P, Fitch and DBRS as long-running political upheaval escalates and risks morphing into a public finances crisis.

The National Assembly has evicted two prime ministers in the last year over their budget plans after snap elections split the house into irreconcilable minority groups. The latest premier, Sebastien Lecornu, has only managed to remain in office by ceding to pressure from opposition lawmakers to suspend President Emmanuel Macron’s pension reform that aimed to bolster public finances.

Moody’s warned that if the suspension of the reform — which raises the minimum retirement age to 64 from 62 — lasts beyond a few years it will further increase fiscal challenges and harm the economy’s potential growth.

Even after suspending the pension reform, Lecornu remains vulnerable as the Socialists, whose support he relies on to stay in power, are threatening to join no-confidence votes if the government doesn’t make more concessions on the 2026 budget. Their core demands include less spending cuts and a significant increase in taxation on the wealthy and large businesses.

Adding to the fiscal uncertainty, Lecornu has relinquished using a constitutional tool known as Article 49.3 that previous governments relied on to bypass votes on the budget when they did not have an absolute majority. It is unclear how fractious lawmakers will be able to agree on a bill at a time when unpopular spending cuts or tax increases are needed to get a grip on a runaway deficit.

“It is no longer possible to govern by the discipline of one camp alone, but by the cultivation of a rigorous debate between lawmakers who start with different beliefs,” Lecornu said earlier Friday at the National Assembly. “It’s parliament’s quiet revolution.”

The initial draft bill Lecornu submitted to parliament this month targets a reduction in the budget shortfall to 4.7% of economic output from 5.4% this year. But he has said lawmakers have latitude to negotiate a wider objective, so long as the deficit remains within 5% and France can still meet its longer term goal of 3% by 2029.

The country’s finance minister, Roland Lescure, said after the ratings decision that the government remains committed to an “ambitious” reduction in the deficit to meet the 2029 goal. The rating firm’s negative outlook shows the “absolute necessity” for a compromise on the budget, he added.

“If persistent, the inability to pass legislation that effectively addresses such policy challenges would mark a weakening of the country’s institutions,” Moody’s said. “In the absence of budgets that would pro-actively contain spending or raise revenue, France’s deficits would remain wider for longer than we currently expect.”

Commenting in an interview with La Croix published Saturday, Bank of France Governor Francois Villeroy de Galhau warned lawmakers debating the 2026 budget that the deficit must be no greater than 4.8% of economic output to ensure the country can tackle its growing debt burden.

“It is absolutely necessary to get within 3% between now and 2029 and this means a maximum deficit of 4.8% next year to cover a quarter of the path,” he was cited as saying. “The 3% is not just a European rule — it’s above all the threshold to finally stabilize public debt.”

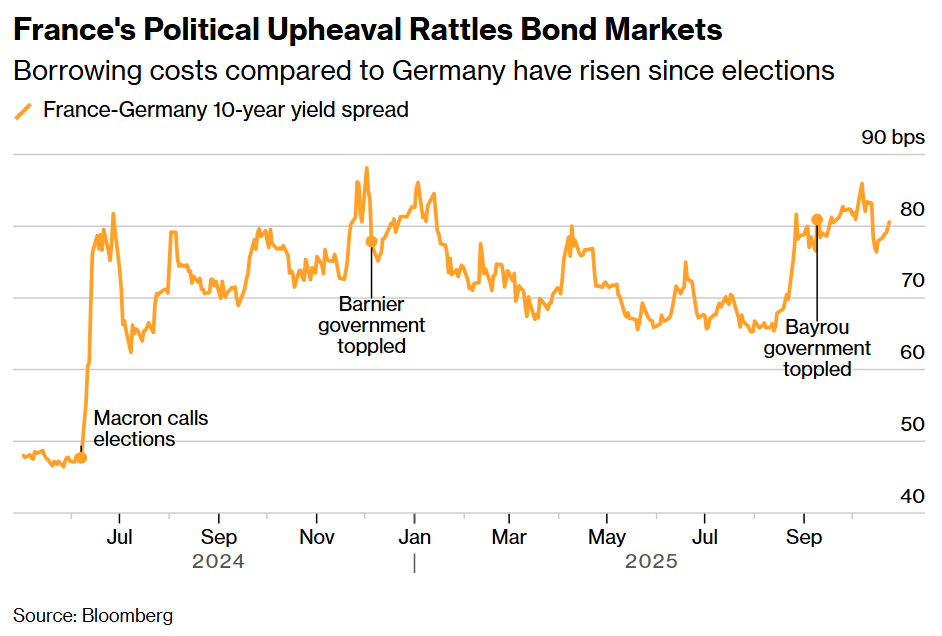

Political and fiscal challenges since Macron called elections in June 2024 have triggered sell-offs of French assets, driving up the country’s borrowing costs.

The spread between 10-year French and German yields, a closely-watched risk metric, rose as high as 89 basis points in recent weeks from fewer than 50 before the snap vote. On Friday, it closed at 81, the highest in 11 days.

S&P’s unscheduled downgrade last week added to selling pressure as it meant France lost its average double-A rating from the three major credit-rating agencies, triggering forced sales among a number of funds with ultra-strict investment criteria. Others have rushed to change their investment rules so they don’t need to reduce their holdings.

Moody’s decision to put a negative outlook on France comes less than a year after it downgraded the country in an unscheduled decision. But the move was broadly expected by investors, given the rising hurdles to fiscal consolidation and recent downgrades from other firms.

Moody’s said a downgrade of France would likely result from further signs the country’s ability to tackle credit challenges has “durably weakened.” This could be evidenced by continued difficulties containing the deficit or a lasting pause or reversal in structural reforms, particularly concerning pensions, it said.

“Moody’s is the only agency where France still has a double-A, which shows that our country has assets,” Villeroy said in the interview with Le Croix. “But all the agencies are alarmed by the political instability, and our serious budgetary problem.”

Written by: William Horobin @Bloomberg — With assistance from Greg Ritchie

The post “France Gets Fresh Warning on Debt as Moody’s Turns Negative” first appeared on Bloomberg

{kind=link}

{kind=link}