A series of large sales in US Treasury futures exacerbated a selloff in the $31 trillion government debt market, as concern about resurgent inflation pushed investors to price in higher interest rates.

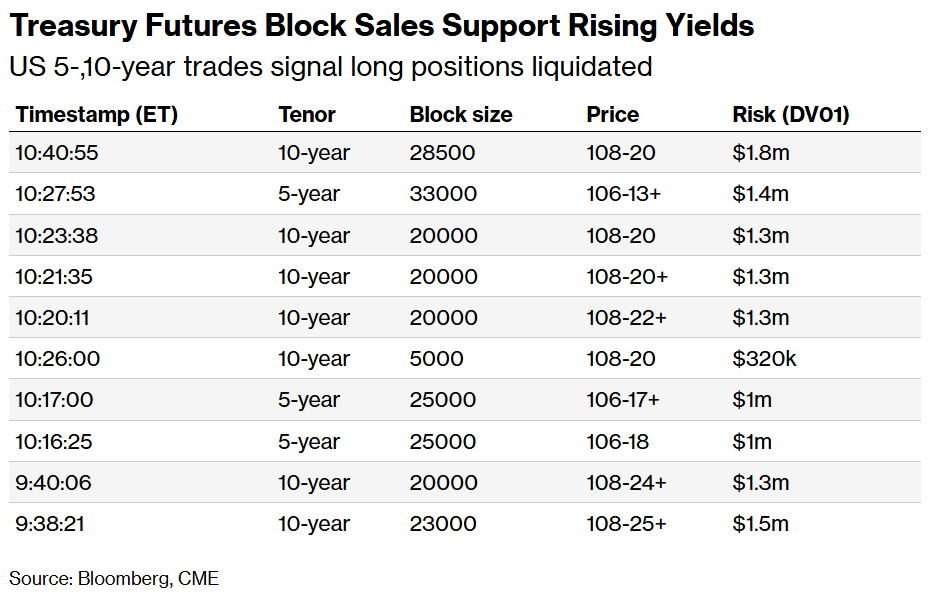

As long-end yields soared to their highest level since 2007 on Tuesday, a wave of block sales in both 5- and 10-year note futures added to the pressure. The futures transactions — which came during a manic hour of trading in the US morning session — were equivalent to roughly $15 billion of the current cash 10-year note, according to data compiled by Bloomberg.

It was a “capitulation-type day in Treasuries,” said Alan Taylor, Founding Partner at Archr LLP, adding that the selloff was accelerated by “multiple block sellers.”

The selling was the latest evidence of how a war-fueled jump in energy prices is adding to inflation fears and driving bets that central banks, including the Federal Reserve, will need to raise interest rates. Futures on Tuesday reflected an 85% chance of a rate increase by year-end, compared to no pricing of a hike reflected on May 1.

Persistently higher yields threaten to slow the US economy, which has so far proved resilient, and lift borrowing costs for US home buyers and corporations.

The first of Tuesday’s big blocks hit the market at 9:38 a.m. New York time and was followed by steady selling until around 10:40 a.m. The roughly one-hour stretch saw 136,500 10-year note futures sold via block trades with 83,000 5-year note futures. Volumes in 10-year notes was around 80% above its 20-day average.

The trades amounted to a combined risk weighting of approximately $12 million per basis point over ten blocks. Transactions in these contracts are anonymous, making it difficult to identify the firms involved and the exact beneficiaries of the bets.

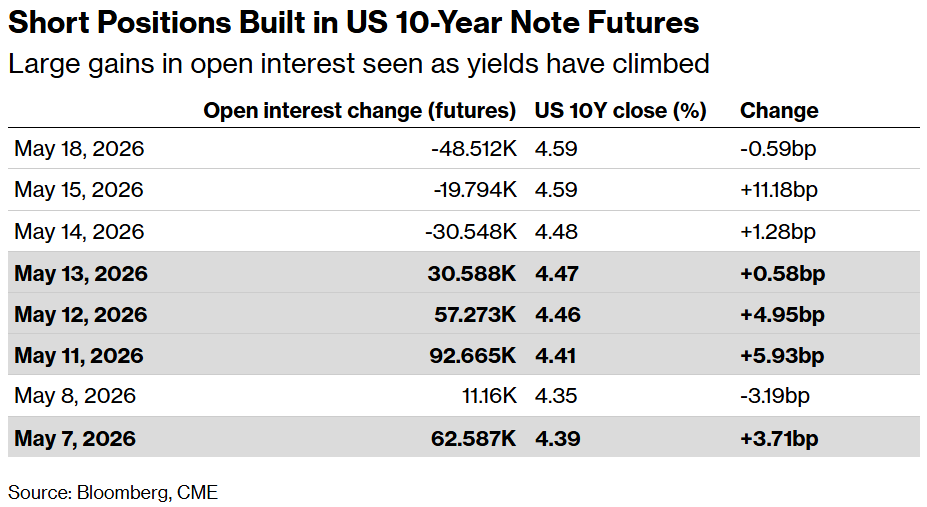

While Tuesday’s activity likely stemmed from traders liquidating bullish wagers, market positioning over the last several sessions has increasingly leaned bearish. Last week, open interest data reflected the build-up of new short positions, with traders adding risk in 10-year note futures as yields started to climb.

There has been a “large addition of new short risks into the cheapening over the last five days,” Citi strategist David Bieber said. He added that short positioning is now “highly extended” both tactically and structurally.

In Treasury options, the sale of an August 10-year put on Tuesday appeared to kick off a spree of profit-taking by a trader who purchased bearish puts back in April. There has also been recent demand to fade the bond market selloff: One trade seen Monday looked to target a move in 10-year yields back down to 4.45% by the end of this week.

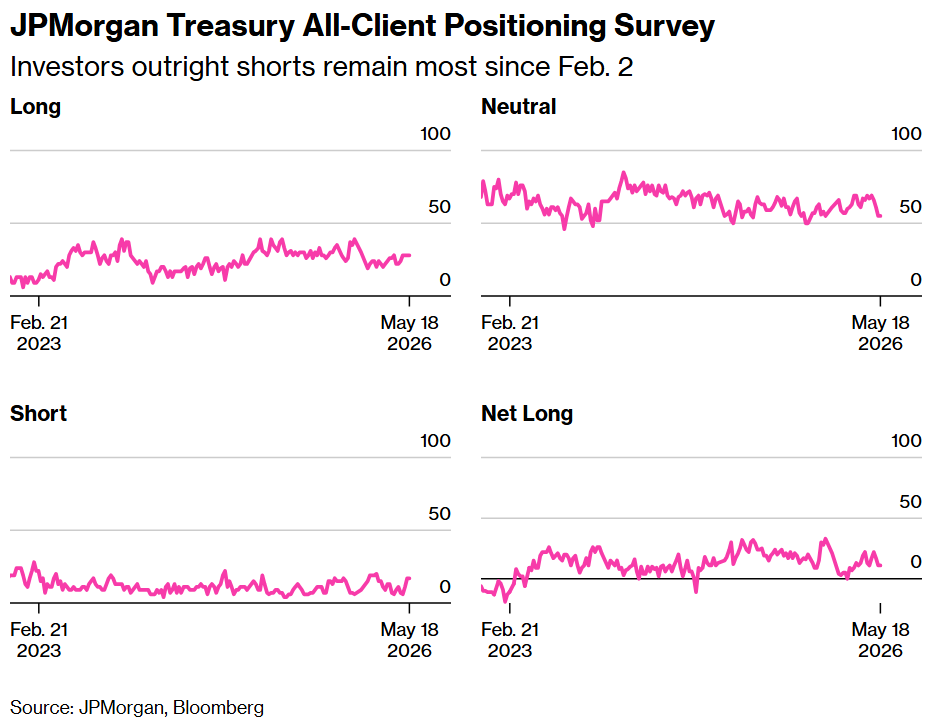

In the cash market, a survey of JPMorgan Treasury clients was unchanged over the latest week, meaning outright short positions remained at the most elevated in over three months.

Here’s a rundown of the latest positioning indicators across the rates market:

In the week up to May 18 investor position was unchanged, with the outright short positions remaining at the most since the start of February.

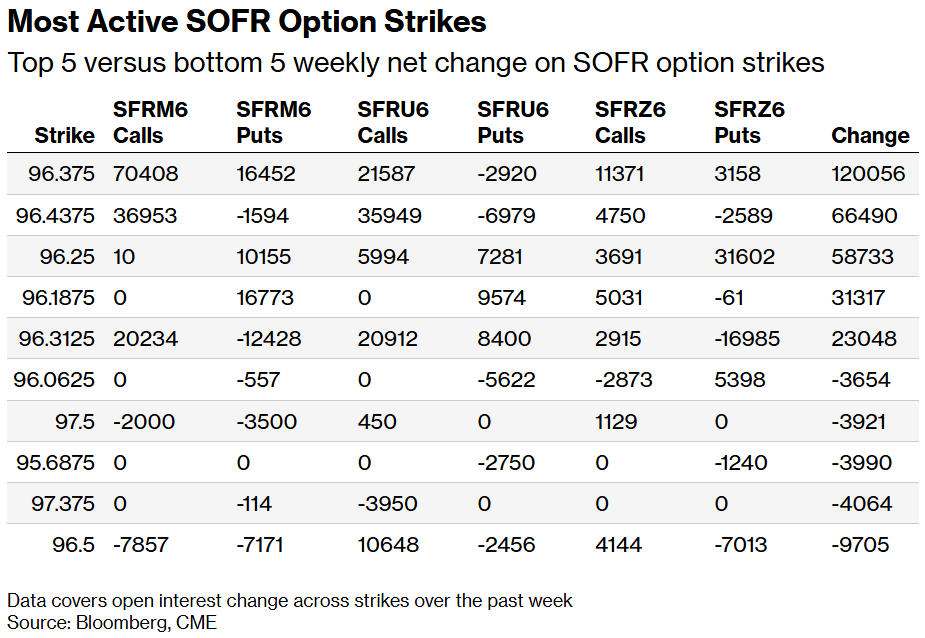

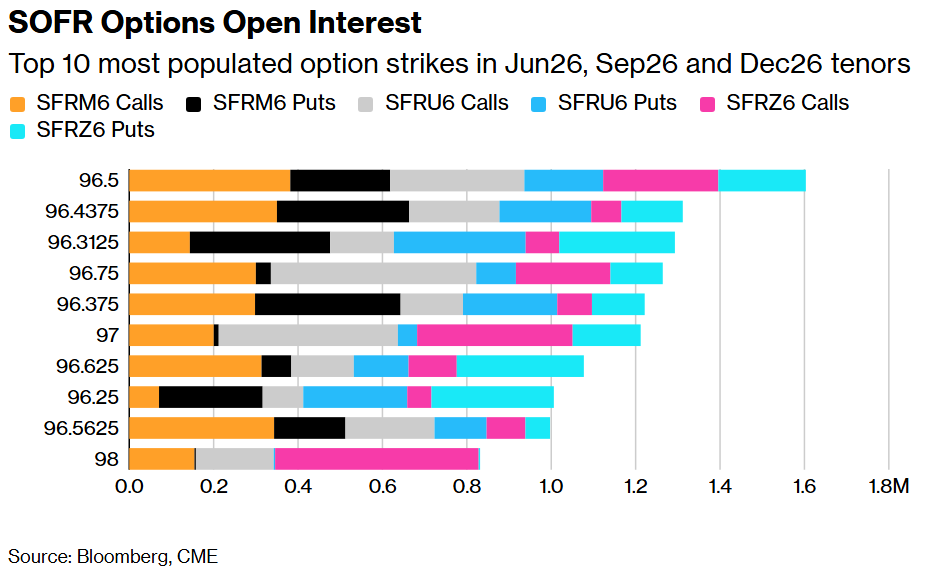

Across SOFR Jun26, Sep26 and Dec26 options, open interest rose the most in 96.375 and 96.4375 strikes due to a large amount of Jun26 call risk added via heavy buying of the SFRM6 96.3125/96.375/96.4375 call fly.

The 96.50 strike remains the biggest populated position across Jun26, Sep26 and Dec26 options, followed by the 96.4375 after a large amount of Jun26 call risk was added via 96.3125/96.375/96.4375 call flies, which traded in heavy size last week. The 96.3125 strike remains well populated also where open interest has grown over recent weeks. Flows have included buyer of SFRU6 96.3125/96.4375/96.5625 call flies. There remains a decent amount of open interest in the 96.75 strike, where a large amount of risk can be seen in Jun26 and Sep26 calls.

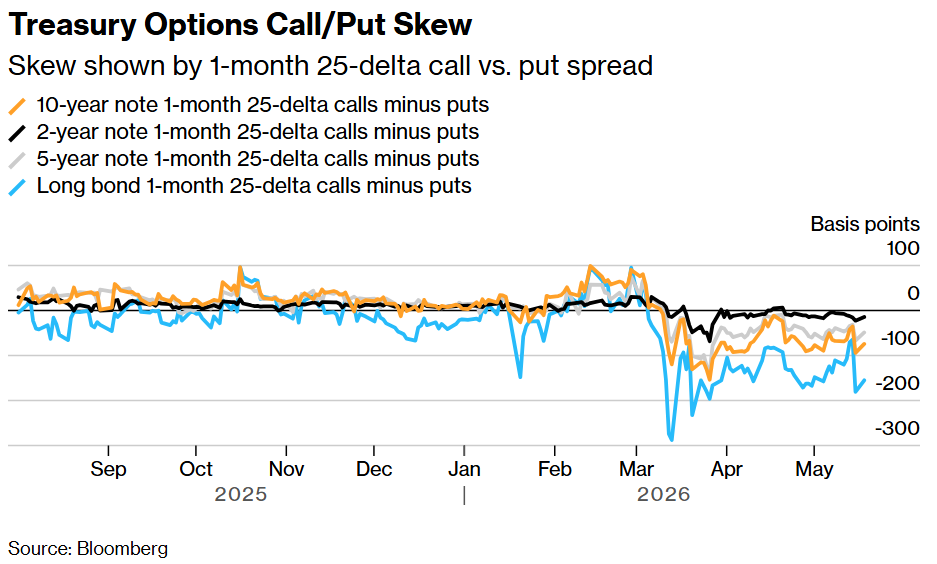

The premium paid to hedge options in the long-end of the curve moved to favor puts over the past week by the most since the end of March. The move came as 30-year yields pushed to 5.15% on Monday and the highest level since October 2023. Treasury options flows on Monday included a buyer of calls in 10-year tenor, looking for a yield move to 4.45% and a large 10-year strangle seller, looking to fade the recent tick higher in rates volatility.

Written by: Edward Bolingbroke — With assistance from Michael MacKenzie @Bloomberg

The post “Big Treasury Block Sales Drive ‘Capitulation’ Selloff in Bonds” first appeared on Bloomberg

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}